Economic Moats Explained: What They Are & Why They Matter - Part I

The beginning of a multi-part deep dive into a foundational concept in quality investing

Flyover Stocks is approaching its first anniversary, and while we’ve discussed moats in several articles and analyzed them for each company profiled, I wanted to create a multi-part series that takes a deeper and more comprehensive look at this foundational topic for quality investors.

In the coming weeks, we’ll cover the following topics (I will add the links to this post as they become available):

Part I: Why Care About Moats? (Today’s post)

Why Care About Moats?

In finance, we often use terms and assume the other person understands what we mean. “Economic moats” has become one of those terms, and having studied the topic for 15 years now, I’ve learned there’s an inconsistent understanding of what we mean when we talk about moats.

I want to return to first principles and illustrate why we should care about economic moats.

Companies invest in tangible and intangible assets using a mix of debt and equity, with the aim of generating profits from those assets. If the assets generate returns in excess of the cost of capital (a mix of debt and equity financing), the company creates shareholder value. If the financing costs outweigh the returns on invested capital (ROIC), the company destroys shareholder value and should stop investing.

In favorable years, some companies can temporarily generate ROIC above the cost of capital, but companies with durable competitive advantages - economic moats - can sustainably generate ROIC above the cost of capital.

To illustrate, consider the 20-year ROIC track records for Fastenal, Hermes, P&G, Jack Henry, and Copart. The black line below represents a generic 9% cost of capital.

As Buffett keenly observed over 40 years ago when he coined the phrase “economic moat,” in a state of perfect competition, the magnitude and persistence of high ROICs would not be possible. Consequently, these companies must have unfair and durable advantages, which form a moat that prevents competition from closing in.

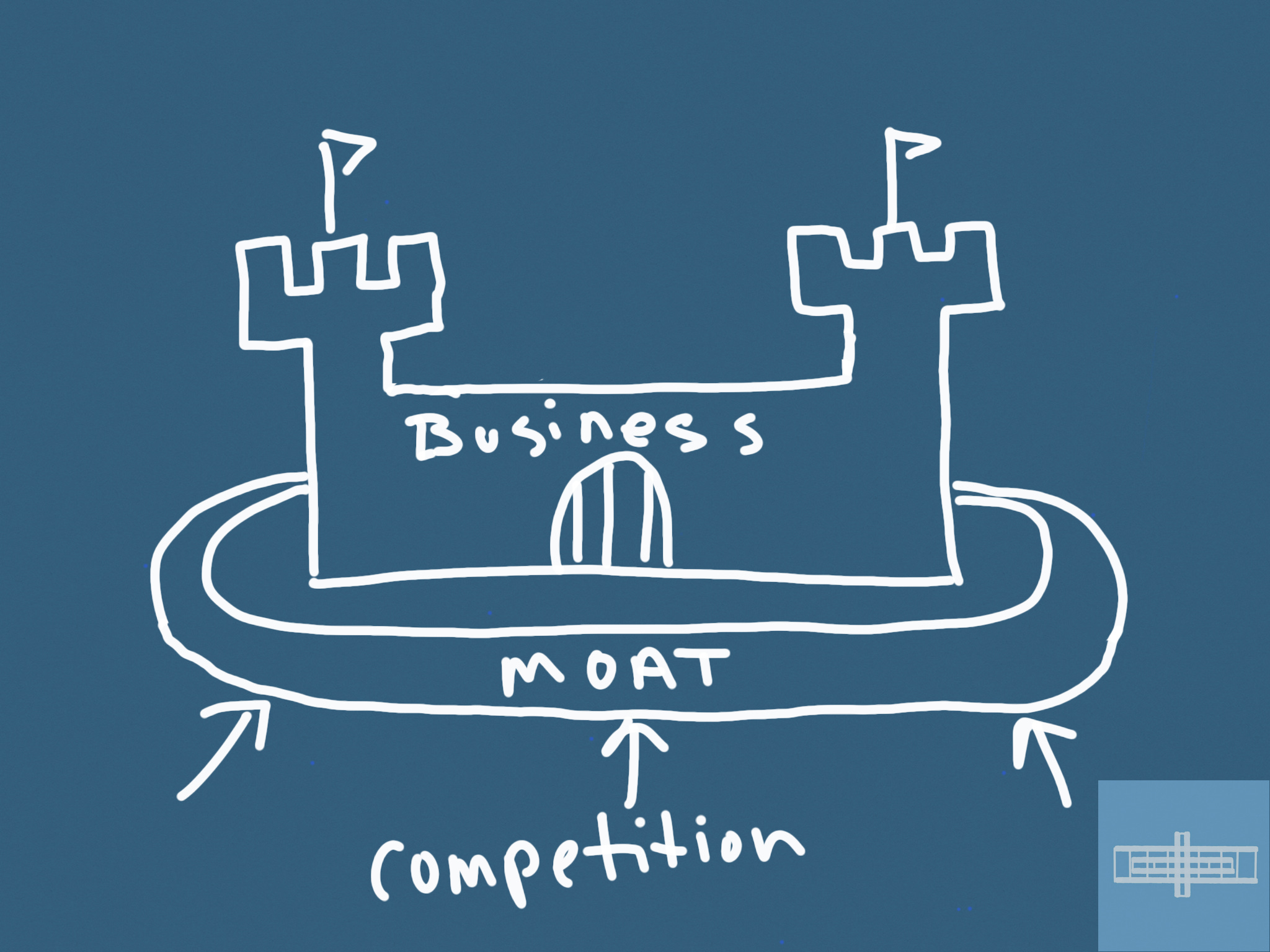

Importantly, a moat is not the economic engine of the business. Instead, a moat's value derives from the castle it's protecting. I'm sure a buggy whip company or two had moats in the early 20th century, but they were worthless once the Model T hit the streets.

Competitors don't attack castle ruins - they're after big, shiny castles. And the bigger and shinier the castle, the wider the moat must be to keep them at bay.

If we want to own quality businesses with superior economics, then we must understand the source of a company's moat, how wide the moat is, how long the moat might persist, if the moat is getting stronger or weaker, and how capable the knight behind the castle wall is at widening the moat. We'll cover these topics in this series in more detail.

Premium fare

Great franchises protected by economic moats naturally attract capital, and companies with persistently high ROIC should, all else equal, command premium multiples to lower ROIC peers.

Here’s why. Consider two peers—Company A generates 20% ROIC, and Company B 10%. If both companies can grow earnings at 10% per year, Company A only has to reinvest 50%, while Company B has to reinvest all of its earnings. This leaves Company A with remaining cash flow to return to shareholders via dividends, buybacks, and debt reduction. It’s a more attractive asset as it has more distributable cash flow.

To be sure, companies with economic moats are not always good investments. Market prices sometimes imply unreasonably high expectations, and returns can be diminished by contracting multiples, even if you’re right about the business’s fundamentals.

Risks and opportunities

Moats can also have risks. The most important one to watch for is complacency. Moats have a way of making those behind the castle walls a bit too comfortable.

As companies gain success and scale, bureaucratic fiefdoms have a way of popping up behind the moat, preventing necessary innovation and becoming culturally insular. Kodak is the classic example, as the company patented digital camera technology but didn’t want to kill its cash-cow film business.

Indeed, moat erosion starts behind the castle walls.

The upsides of owning companies with economic moats, however, far outweigh the risks. Among other things, companies with economic moats:

Tend to attract talented employees who can better serve customers and further widen the moat.

Provide management time to respond to challenges that weaker competitors don’t have.

Can press their advantages in downturns, strengthening them at the start of the next cycle.

Finally, companies with moats better lend themselves to patient holding. Not only do they perform better as a group in downturns, but when they are acquired at a reasonable price, you can let the fundamental compounding do most of the legwork. By comparison, no-moat companies must be acquired at deep discounts and should be flipped when the valuation gap closes.

Bottom line

Not every investor or investment style needs to prioritize investing in companies with economic moats, but investors that prioritize owning quality businesses and holding them patiently should absolutely understand how to analyze moats and how management can enhance or destroy them.

I hope you’ll follow along with the rest of the series.

Stay patient, stay focused.

Todd

Todd Wenning is the President and CIO at KNA Capital Management, LLC, which is pending state registration.

Todd can be reached through this contact form.

At the time of publication, Todd, his family, and/or KNA Capital Management did not own shares of any company mentioned.

All information contained herein is provided “as is” and KNA Capital Management, LLC (“KNA”) expressly disclaims making any express or implied warranties with respect to the fitness of the information contained herein for any particular usage, application or purpose. Prior to making any investment decision you should consult with professional financial, legal and tax advisors to determine the appropriateness of the risks associated with such an investment. No assurance can be given that the objectives of a particular investment will be achieved or that an investor will receive a return of all or part of his or her investment. All investments involve the risk of loss, including the loss of principal. In no event shall KNA be responsible or liable for the correctness of any material used herein or for any damage or lost opportunities resulting from the use of such material.

Users of this content may not reproduce, modify, copy, alter in any way, distribute, sell, resell, transmit, transfer, license, assign or publish any information obtained through this website without permission. KNA and the terms, logos, and marks included herein that identify KNA products are proprietary materials. The use of such terms, logos, and marks without the express written consent of KNA is strictly prohibited.

Disclaimer:

Todd is the President and CIO of KNA Capital Management, LLC, an investment management firm based in Cincinnati, Ohio that is currently pending state registration. The information contained on this site as well as kna-capital.com is for informational purposes only and should not be considered as investment advice or as a recommendation of any particular strategy or investment product. This blog should not be considered as a solicitation for services.

This material on FlyoverStocks.com is published by W8 Group, LLC and is for informational, entertainment, and educational purposes only and is not financial advice or a solicitation to deal in any of the securities mentioned. All investments carry risks, including the risk of losing all your investment. Investors should carefully consider the risks involved before making any investment decision. Be sure to do your own due diligence before making an investment of any kind.

At time of publication, the author, his family, or KNA Capital Management clients may have an interest in the securities mentioned or discussed. Any ownership of this kind will be disclosed at the time of publication, but may not be updated if ownership of a particular security changes after publication.

This newsletter does not provide buy or sell recommendations and articles should not be interpreted this way.

Information presented may be sourced from third parties and public filings. Unless otherwise specified, any links to these sources are included for convenience only and are not endorsements, sponsorships, or recommendations of any opinions expressed or services offered by those third parties.

Flyover Stocks has partnered with Koyfin to provide a discount to Koyfin’s services for Flyover Stocks readers. The W8 Group, LLC, which publishes Flyover Stocks, may receive a commission from a reader’s purchase of products linked from this page as part of an affiliate program.

Well done, Todd!