Economic Moats Explained: What They Are & Why They Matter - Part V

How to assess whether a company's moat is getting wider or narrower

For the fifth part of this series, we’ll explore moat trend.

I encourage you to read Parts I-IV before reading this post.

Part I: Why Care About Moats?

Part II: Moat Sources

Part III: Moat Width

Part IV: Moat Depth

Part V: Moat Trend (today’s post)

Part VI: How Management Impacts the Moat

Companies are not static assets. Unlike gold or artwork, companies are always changing. Future cash flows are unknown.

It’s true that some companies change slower than others, but eventually, every current employee will retire or leave and a new crop will take over. Every asset will break down or become obsolete and need to be replaced or refreshed. A company you invested in 10 or 20 years ago is not the same company today.

What’s more, companies are in a constant battle against entropy: the natural tendency toward disorder and decay. Just staying in place takes effort.

Given the constant state of change and the weight of entropy, it’s remarkable that some companies are able to dig a moat in the first place. Those that are able sustain it - and even widen it - are in a special class indeed.

The direction of a company’s moat - widening or narrowing - is a product of daily decisions by both managers and employees. Buffett touches on this point in one of my favorite passages from his letters. This from the 2005 shareholder letter:

“Every day, in countless ways, the competitive position of each of our businesses grows either weaker or stronger. If we are delighting customers, eliminating unnecessary costs and improving our products and services, we gain strength. But if we treat customers with indifference or tolerate bloat, our businesses will wither. On a daily basis, the effects of our actions are imperceptible; cumulatively, though, their consequences are enormous.

When our long-term competitive position improves as a result of these almost unnoticeable actions, we describe the phenomenon as “widening the moat.” And doing that is essential if we are to have the kind of business we want a decade or two from now. We always, of course, hope to earn more money in the short-term. But when short-term and long-term conflict, widening the moat must take precedence.” (my emphasis)

As outside investors, it’s hard for us to notice these daily micro actions. (Once in a while, though, we might pick up on something.)

Heck, it’s even hard for board members and executives to notice them, especially when a company is spread out over many geographies.

But, as Buffett observed, the cumulative effects of these daily actions have enormous consequences to the moat. At a minimum, we should be on the lookout for discernable trends.

The effects eventually show up in the form of stronger pricing power, lower costs, or ideally both. As a result, returns on incremental invested capital (ROIIC) improve, and the business grows intrinsic value at a faster pace. In turn, the market typically rewards the company with a higher share price.

Chutes and ladders

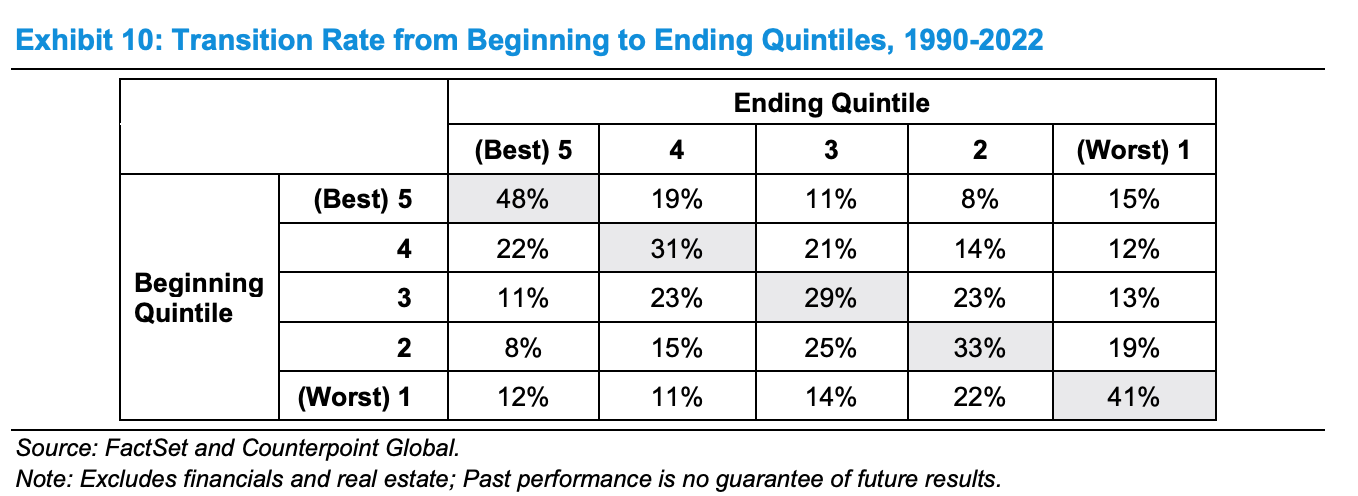

Of course, this works in both directions. In Michael Mauboussin and Dan Callahan’s excellent 2023 paper called “ROIC and the Investment Process”, the authors show how over rolling three-year periods from 1990 to 2022, cohorts of companies that moved up ROIC quintiles exhibited more positive total shareholder returns. In contrast, those that slipped quintiles posted relatively poor returns.

Fortunately, as the accompanying table shows, companies in the highest ROIC quintile tend to stay in the highest quintile, but if a company falls out of the highest quintile, it is more likely to have poor subsequent performance. We discussed this at more length in this video on quality traps.

Given the tendency of companies to perform better when ROIC meaningfully improves and perform worse when ROIC meaningfully declines, it pays to understand how moat trend can impact changes in ROIC.

Evaluating moat trend

Ultimately, what we’re trying to determine with moat trend analysis is “Are the company’s identifiable competitive advantages getting stronger or weaker over the next three to five years?”

Before evaluating moat trend, we need to understand the sources of the company’s moat, such as low-cost production, network effects, switching costs, intangible assets, or efficient scale. (We explored each of these moat sources in Part II of this series.)

Once you’ve identified the source of the company’s advantage, you can better evaluate its direction.

This is, in fact, what Buffett did when describing GEICO in the 1986 letter to Berkshire Hathaway shareholders:

“The difference between GEICO’s costs and those of its competitors is a kind of moat that protects a valuable and much-sought-after business castle. No one understands this moat-around-the-castle concept better than Bill Snyder, Chairman of GEICO. He continually widens the moat by driving down costs still more, thereby defending and strengthening the economic franchise.”Buffett identified the moat source (low costs) and tracked GEICO’s moat trend by evaluating GEICO’s costs (in insurance terms, the expense ratio) relative to those of its competitors.

You’ll note that Buffett ties this relationship to actions taken by then-chairman/CEO Bill Snyder. In the final segment in this series, we’ll explore how management’s actions impact all aspects of the moat.

Having a metric to track helps a great deal in moat trend evaluation. It doesn’t have to be a traditional metric like insurance expense ratio, but the data must be relevant and available.

Two of the metrics I watch at Costco, for example, are Change in Annual Executive Membership and Executive Members as a % of Total Members.

These two metrics provide a regular update on how relevant Costco is to its customers. Here’s why.

You can shop at a Costco with the basic Gold Star Membership (currently $65 per year in the US). The Gold Star Membership gives you access to just about everything Costco has to offer.

Therefore, to justify an upgrade to Executive Membership (currently $130 per year in the US) in which you get a 2% reward on purchases, you need to spend at least $3,250 annually - or $270 per month on average - at Costco to break even with the Gold Star Membership.

With few exceptions, $270 a month implies that shopping at Costco is part of your routine. And as research suggests, once a store is ingrained in your routine, it usually takes a major life event like having a baby or a global pandemic to disrupt it.

The more members spend at Costco, the more bargaining power Costco has with its suppliers, the lower prices it can offer its members, the more members join Costco. As this process plays out, Costco’s moat gets wider and ROIC drifts higher. It shouldn’t be a surprise that Costco’s stock price has followed suit.

What moat trend isn’t

Companies - and particularly cyclical companies - tend to get a ROIC boost in favorable markets. These natural ebbs and flows may impact the stock price, but they do not represent moat trend as they are outside or “systematic” forces.

What we’re after with moat trend is instead company-specific. Indeed, a company’s moat trend can improve in a downswing if its competitors weren’t prepared and the company gains market share.

Growth can be indicative of a moat trend if the growth is adding intrinsic value, but growth alone is not a moat trend, as companies can grow while investing in projects that destroy value.

Changes in business mix are also not in themselves indicative of moat trend. For example, if a company has a wide-moat segment and a no-moat segment and spins off its no-moat segment, the company’s moat trend does not turn positive because only the wide-moat segment remains. What’s more important to understand is if that wide-moat segment is itself building upon its advantages or not.

Moat trend process

As you’re thinking about moat trend at a company, consider the following steps:

Identify the moat source: What’s the source of the company’s competitive advantage? Why does the company benefit from the moat source and why don’t its competitors equally benefit from it?

Find or build metrics to track moat source strength: If the company has a low-cost advantage, are costs per unit declining? If the company benefits from switching cost advantages, is the retention rate or spending per customer moving higher?

Consider medium-term relevance of product or service: Do you expect the company’s offerings to be at least as relevant in five years as they are today? eBay has long been used as a classic example of a network effect moat, but the relevance of online auction platforms declined as local classifieds (Facebook Marketplace, Craigslist) and direct e-commerce (Amazon, Walmart) became more ubiquitous and easier to use.

Cultural impact: Does the company’s corporate culture support or detract from the company’s moat? A company with a weak corporate culture (e.g. revolving door management, multiple private equity owners over the last decade) will be less likely to correct a negative moat trend.

Correctly identifying positive moat trends can lead to strong returns, but if your investment universe is already whittled down to quality, high ROIC businesses, then moat trend analysis is most useful as a way to avoid negative moat trends. As Mauboussin and Callahan’s table above suggests, the companies that start with a top quintile ROIC and drop out of that cohort often have the furthest to fall. These are the aforementioned “quality traps.”

On the other hand, positive moat trends are most useful if you’re looking for companies to move up from lower ROIC cohorts. As discussed in the Hawkins profile from February 2024, the company’s growing competitive strength in water treatment alongside increased relevance of its services pointed toward improving segment margins.

As Hawkins acquires new water treatment facilities and integrates the company into the Hawkins’ way of doing business, I expect segment margins to improve back to the mid-teens and support the company’s overall margin expansion.

Supporting this trend is increased attention being paid toward removing water contaminants like lead and PFAS from municipal water. In addition, reshoring of manufacturing will lead to greater industrial demand.

Thus far, that seems to be playing out in Hawkins’ water segment, and the stock has followed alongside this progress.

Bottom line

Moat trend analysis is a helpful way of framing and tracking the momentum of a company’s competitive advantages. These changes can’t be screened for and require qualitative effort to understand the company at a deep level.

How do you think about moat trend? Please let me know in the comments below.

I’ll conclude this series in a few weeks with Part VI, which looks at the intersection of moat and management. Stay tuned!

Stay patient, stay focused.

Todd

Todd Wenning is the founder of KNA Capital Management, LLC, an Ohio-registered investment advisor that manages a concentrated equity strategy and provides other investment-related services.

At the time of publication, Todd, his immediate family, and/or KNA Capital Management, LLC own shares of Costco, Amazon, and Berkshire Hathaway.

Please see important disclaimers.

Just want to say thank you for this series on Moats. My understanding of moats and my checklist I run investment opportunities through have significantly improved in such a short period of time thanks to you.

Love this. My understanding of MOATS is that its a relative game. So while looking at trends and metrics that could signal a degradation, it seems useful to look at those metrics and how they evolve between the different competitors, looking at the GAP between the companies. If there is a short-term downturn due to external factors, we can spot which company remains the strongest and thus might have the better or more durable MOAT. Lack of growth seems a strong indicator for quality traps unless competitors are slowing down faster.