Economic Moats Explained: What They Are & Why They Matter - Part III

The sufficiency of a company’s moat width is dependent on the size of the castle it’s meant to protect.

Our managers of the businesses we run, I’ve got one message to them, which is to widen the moat. And we want to throw crocodiles and sharks and everything else, gators, I guess, into the moat to keep away competitors. – Warren Buffett

For the third part of this series, we’ll explore moat width.

I encourage you to read Parts I and II before reading this post.

Part I: Why Care About Moats?

Part II: Moat Sources

Part III: Moat Width (today’s post)

Part IV: Moat Depth

Part V: Moat Trend

Part VI: How Management Impacts the Moat

I’m fascinated by companies that have stood the test of time.

There’s a small roofing materials distributor near my house that’s been in business for 149 years. It’s managed by the fourth generation founding family.

As I’ve have travelled around the country with my family, I’ve noticed similarly long-lived independent distributors. The common denominator seems to be deep customer relationships and service track records built over decades.

Local advantages they may be, but they are durable.

Without seeing any of their financials, my guess is that their advantages yield high single-digit returns on invested capital, on average. That’s enough to reinvest in the business and pay the owners a tidy dividend, but not enough to expand regionally, and eventually, nationally.

These advantages haven’t been competed away because upstart local competitors lack the established relationships. Given tight margins in distribution, upstarts would need to take losses for years to compete on service. On the other hand, larger competitors are better off acquiring the company than competing on price and dragging down ROIC for both parties.

It's a nice position for the local incumbents. That said, local distributors can’t press their advantages too far in pursuit of higher margins and ROIC. If that were to happen, competitors would have enough incentive to enter the market.

In other words, their moats aren’t wide enough to support that strategy.

Moat and Castle

In the opening article in this series on economic moats, I wrote:

“Competitors don't attack castle ruins - they're after big, shiny castles. And the bigger and shinier the castle, the wider the moat must be to keep them at bay.”

For the local distributors, a skinny moat is sufficient to protect their impressive, but relatively modest, castles.

That’s not the case for the likes of Google, Visa, or Copart, however. Each of these businesses is a big, shiny castle coveted by competitors. They need wide imposing moats to maintain their position.

The sufficiency of a company’s moat width is dependent on the size of the castle it’s meant to protect.

Whether it’s a wide or narrow moat, the question to ask is, “Will competition size up the castle and say, ‘Eh, not worth the trouble.’?”

Pictures of Bodiam Castle in the U.K. are often used in articles on moats (including this one!) because of its wide moat and untouched castle. Indeed, most moated castles are in ruins, but that’s a story for another day.

Historians have debated whether Bodiam’s moat served ornamental or military purposes, but it could be both. It’s situated on the River Rother in East Sussex and it stands to reason that its strategic location could have been attacked, particularly during the War of the Roses.

Yet it wasn’t.

The catch is that as wide as Bodiam’s moat is, it is not particularly deep - about five feet in most parts and could have been besieged with some effort, but if you were a general sizing it up, why would you want to deal with a moat like that in the first place? Your advance would at least have been dramatically slowed.

You can think of moat width as a deterrent of sorts.

Moat depth, which we’ll explore in the next post, considers how durable the moat is to withstand an attack. In other words, how likely is it that the moat will be at least as wide in a decade?

But here, we want to understand how formidable the company’s current advantages are and if they are sufficient to deter competition.

The crown jewels

The attractiveness of the castle depends on the strength of the underlying business. As we discussed in this post on The Warren Buffett Way, a business franchise “possesses the economic goodwill necessary to raise prices in all environments without commensurate capital expenditures, particularly during inflationary ones.”

It's the dream of every business to become a franchise and raise prices as necessary without having to “hold a prayer session” beforehand. Such franchises are natural targets for competitors who want to wear the crown themselves.

As a result of their advantages, wide moat companies tend to have higher and/or more persistent returns on invested capital.

Without a wide moat, the franchise is vulnerable to competition. Raising prices gets harder, more investment is required to keep pace, and returns on invested capital naturally decline.

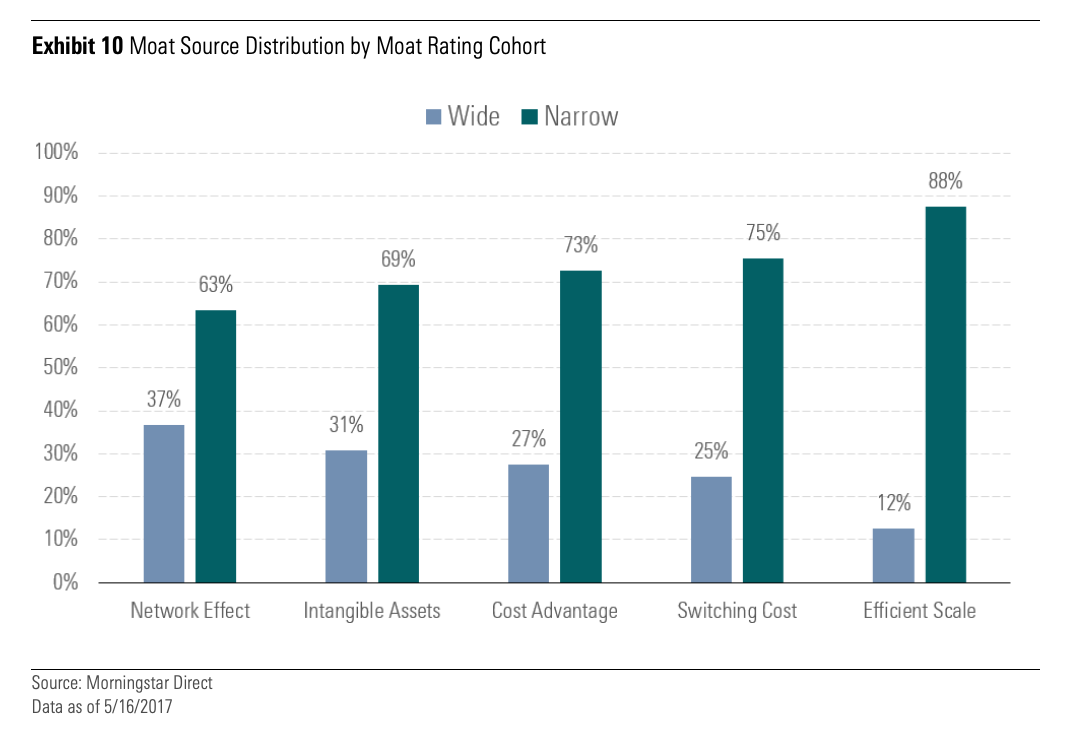

Moat source matters

The nature of the moat source can also tell us something about moat width.

As the below chart from Morningstar shows, network effects are more often found in companies they’ve rated “wide moat” than efficient scale advantages.

That makes sense. Network effects tend to produce “winner take all” or “winner-take-most” industries that result in concentration and little competition.

While network effects can unravel more quickly than other moat sources, when they are supporting a highly-relevant product or service, they are near-impossible to overcome as a competitor.

Efficient scale, in contrast, relies on rational competition to work. If an irrational competitor enters the market and cuts prices to win business, the returns on invested capital and the efficient scale moat source itself dissolve for all participants.

Multiple moat sources

Companies with wide moats also tend to have multiple moat sources.

To illustrate, Copart, which is a global automobile auctioning and remarketing platform, has a number of moat sources behind its wide moat. For one, it has both physical and digital network effects. Its physical network effects come from its storage yards scattered across the country, where it collects damaged cars for auction. The more locations it has, the easier it is for sellers (like insurance companies) to get cars into the Copart system. Copart’s digital network effects are built upon this physical network advantage. As Copart’s inventory grows, the more attractive its online auction platform becomes to both sellers and buyers.

In addition to these network effects, Copart has some intangible asset advantages related to its deep relationships with insurance companies who rely on Copart to help them sell damaged vehicles and minimize their losses.

Because Copart owns rather than leases most of its land, and held much of it for decades, it also has a cost advantage versus competitors just starting out or legacy competitors like IAA who have historically leased their land and are subject to lease negotiations.

Each of Copart’s moat sources are robust on their own and are even more formidable when combined. It has considerable bargaining power with both customers and suppliers and has become an integral part of how the auto insurance industry operates in the United States.

By comparison, Toro has a weaker franchise than Copart; however, a less impressive set of moat sources is sufficient to protect its more modest castle.

Toro’s moat relies on its extensive dealer network that offers professional customers like golf courses, landscapers, and municipalities superior sales and service. For these customers, equipment downtime is lost money and having local service is worth paying a premium for the Toro brand relative to a cheaper brand that doesn’t have a local presence.

Bottom line

Once you’ve determined the quality of the underlying business, you can better understand the width of the moat necessary to defend the company’s position.

Wide moats are as rare as exceptional companies. There might be a few dozen - maybe 100 - in the world. If you’re only looking for wide moats and exceptional companies, your universe may be too restricted. There are great businesses worth considering that are just as well protected by narrow moats. What matters is that the width of the moat matches the attractiveness of the castle it’s defending.

Stay patient, stay focused.

Todd

At the time of publication, Todd, his immediate family, and/or KNA Capital Management owned shares of Howdens Joinery, Medpace, and Worthington Enterprises.

Please see important disclaimers.