What Public Markets Can Teach Founders About Building Durable Businesses

Moats, capital allocation, and stewardship aren’t public market concepts - they’re business fundamentals.

“I’m a better businessman because I’m an investor, and a better investor because I’m a businessman.” - Warren Buffett

Public companies are often seen as the “end state” for a startup or private company. They are viewed as an opportunity to cash out via IPO and maybe turn the reins over to someone else.

But that framing misses something important.

So, what lessons can small business owners, entrepreneurs, and early-stage investors take from the public markets?

Capital allocation, widening the moat, and stewardship aren't just public market concerns - they are core requirements of any business built to last.

In late October, I shared this perspective with Northern Kentucky’s startup community at SparkHaus - a beautiful new entrepreneurship hub and coworking space in Covington.

(Please note that this presentation was given under the KNA Capital Management banner, my Ohio-registered RIA. See important disclaimers.)

The lines between the public and private markets are increasingly blurred, and both sides could learn something from the other. Having studied the public markets for over 20 years, I focused my presentation on three key lessons for entrepreneurs and early-stage investors.

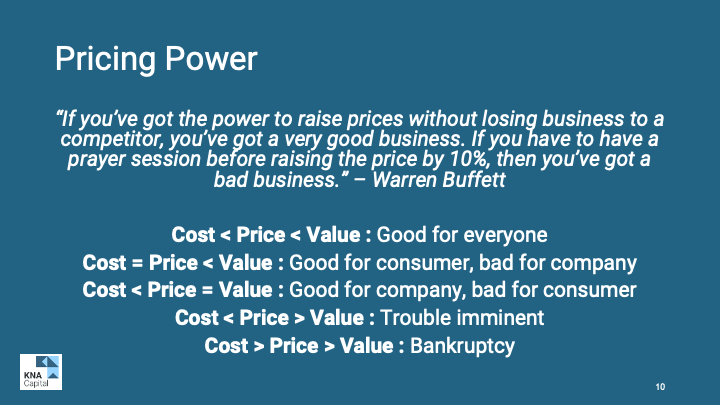

Identify your moat source: What is your unfair advantage? (If you can’t clearly answer this, your competitors eventually will.)

Reinvest capital intentionally: Widening the moat is what ultimately drives higher valuations. (Growth + moat expansion compounds cash flow over time.)

Embrace stewardship: Ensure the business can thrive beyond your tenure. (If it depends entirely on you, it isn’t durable.)

The companies that endure and compound value over time are the ones that execute on these principles.

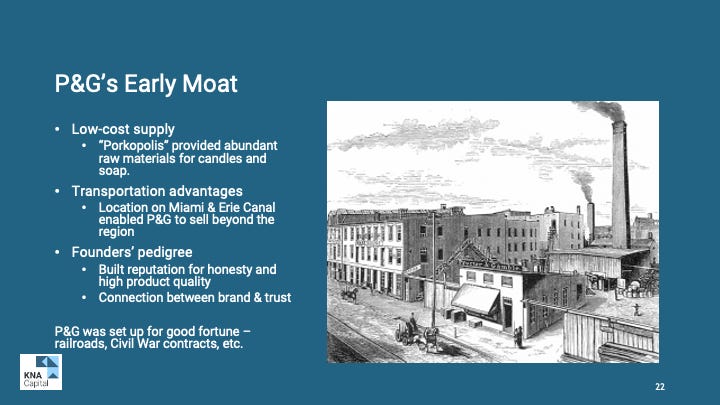

Two of my favorite slides featured historical examples from two of our region’s most successful businesses: Procter & Gamble and National Cash Register.

While these examples are over 100 years old, they illustrate that moats aren’t just for blue chip, publicly-traded companies. Their success began long before a single share traded on an exchange.

What stood out to me about P&G and NCR wasn’t just their success, but their founders’ intentional approach to value creation. They identified their moat sources early and relentlessly invested behind them. They doubled down on what their competitors couldn’t replicate and widened the gap over time.

Finally, we talked about how moats crumble in the public markets and lead to impaired valuations.

Contrary to popular belief, competitors don’t destroy moats - they expose the damage that’s already been done.

Moats actually crumble from the inside-out.

The opportunity for competitors to attack starts with internal complacency or misaligned incentives.

The fastest way to destroy your successful business isn’t external competition, it’s “mortgaging your moat.” Companies can mortgage their moat by failing to provide enough consumer surplus (the gap between their product’s price and the consumer’s perceived value).

Ultimately, the public markets offer business owners and investors at all stages timeless lessons of what creates and destroys value.

Using these three lessons, small business owners and private market investors can increase their business’s value - and potentially become public market success stories themselves.

You can view the full presentation here:

It was a privilege to share these lessons with the Northern Kentucky startup community. If you're building or allocating capital and thinking about the durability of your business, I’d welcome the conversation.

Stay patient, stay focused.

Todd

Todd Wenning is the President & CIO of KNA Capital Management, LLC, an Ohio-registered investment advisor that manages a concentrated equity strategy and provides other investment-related services.

At the time of publication, the author, his immediate family, and/or KNA Capital Management, LLC or its clients do not have positions in any company mentioned.

Please see important disclaimers.

This is such an underexplored angle. Public markets reward durability, but most startup culture optimizes for speed and growth at all costs. Founders who study how enduring public companies think about competitive moats, capital allocation, and long term value creation end up building businesses that actually survive past the hype cycle. More founders should be reading annual reports instead of Twitter threads.