Quality Trap or Buying Opportunities? IBP and MTD Updates

When a falling price is an opportunity, and when it isn't

Todd Wenning is the founder of KNA Capital Management, LLC, an Ohio-registered investment advisor that manages a concentrated equity strategy and provides other investment-related services.

At the time of publication, Todd, his immediate family, and/or KNA Capital Management, LLC or its clients own shares of Copart.

Please see important disclaimers.

How many times have you thought something like this?

“Wow, what a great company. I’d love to buy it, but 35 times earnings? That’s pricey. I’ll wait until it’s trading for 20 times earnings.”

So you wait and then for some reason, the stock sells off and it’s finally trading for 20 times earnings.

The buying opportunity you’ve been waiting for…right?

The answer depends on if this is a quality trap or a market overreaction.

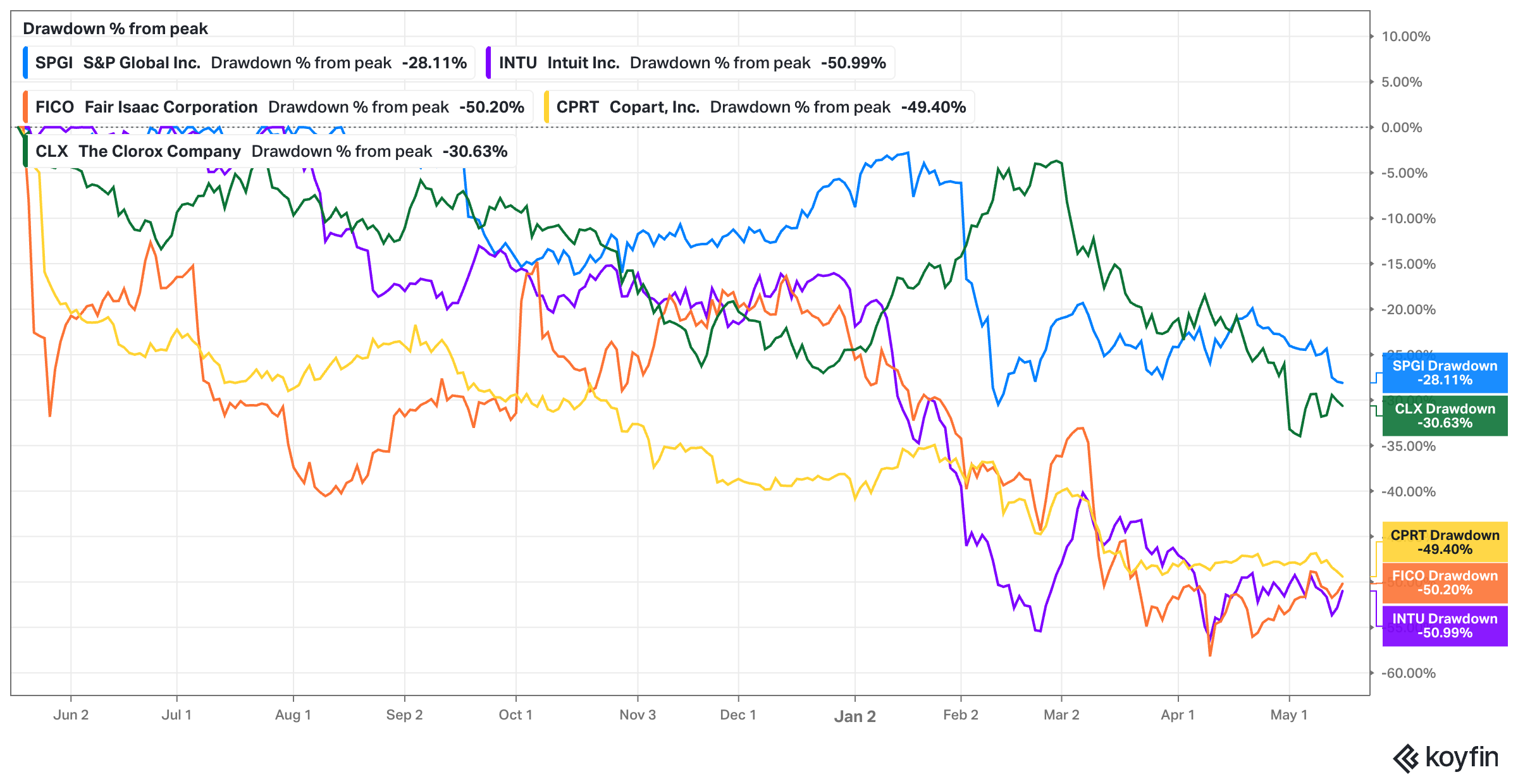

There are a lot of opportunities like this today. Many former high-flying quality companies are now trading for 30%, 40%, or even more, off of their previous highs.

Here are just a few: S&P Global (SPGI), Intuit (INTU), Fair Isaac (FICO), Copart (CPRT), and Clorox (CLX). Just a few years ago, all were considered market darlings among quality-focused investors.

As we’ve discussed, quality traps are the biggest risk for quality-focused investors. These are cases where we pay a premium valuation for what we perceive to be a quality company, only for that multiple to diminish due to a narrowing moat.

Michael Mauboussin and Dan Callahan’s research found that companies that start in the top quintile (as a cohort) of ROIC have the worst subsequent performance if they don’t stay in the top quintile over the next three years.

That’s because what typically occurs is contracting multiples and slowing earnings growth - an inverse “Davis Double Play.” You think you bought a ruby, but what you actually bought was a rhinestone.

Reversion to the mean is a powerful force and great companies must continue to find ways to resist the gravitational pull toward mediocrity.

But sell-offs in quality companies can also be generational buying opportunities when the concerns are priced as secular risks even though they are actually cyclical risks.

Knowing the difference is hard and requires a deep understanding of the company’s competitive position (economic moat), management team (stewardship), cultural ability to respond to challenges, and the underlying value of the business.

One question you must ask yourself when evaluating drawdowns of quality companies is, “Do I think this company’s products and services will be at least as relevant 10 years from now as they are today?”

It’s a hard question to answer, especially for companies whose sell-offs are driven by rapid AI improvements, but that’s the point. Pull the threads necessary to evaluate that question and you’ll steer yourself in the right direction.

Two previously-profiled Flyover Stock companies - Installed Building Products and Mettler-Toledo - are currently in 38% and 32% drawdowns, respectively. Below, I provide updates on my thinking for both companies.