Worthington Industries Spin-Off Update

Thoughts from Worthington's recent investor day ahead of the December spin off of the steel business

Executive summary

Worthington Enterprises - the name of the RemainCo - held an investor day on October 11 that provided insights into the new company’s moat, capital allocation priorities, and growth opportunities.

Assuming a low EV-to-Sales multiple for Worthington Steel (SpinCo), Worthington Enterprises would need to perform poorly for the implied market value to prove expensive.

Worthington Enterprises’ management team has a track record of shareholder value creation, is starting with an investment-grade balance sheet, and is pursuing an asset-light business model.

“We fundamentally believe that investors care about three things, growth, return on invested capital and free cash flow.” - Andy Rose, Worthington Industries CEO

A few weeks ago, Worthington Industries announced that it would accelerate its spin-off of the legacy steel business to late 2023. Ahead of the spin, the two companies held a joint investor day on October 11 to provide investors with more information about their plans as separate entities.

As discussed in the original post, my interest is in the RemainCo - the newly named Worthington Enterprises - which focuses on building products, consumer products, and sustainable energy applications. That’s what we’ll focus on today.

(When I mention “Worthington” going forward, I mean the RemainCo. References to “Worthington Industries” refer to the present, pre-spin company. Unless otherwise noted, all slides included below are from the October 11, 2023 presentation.)

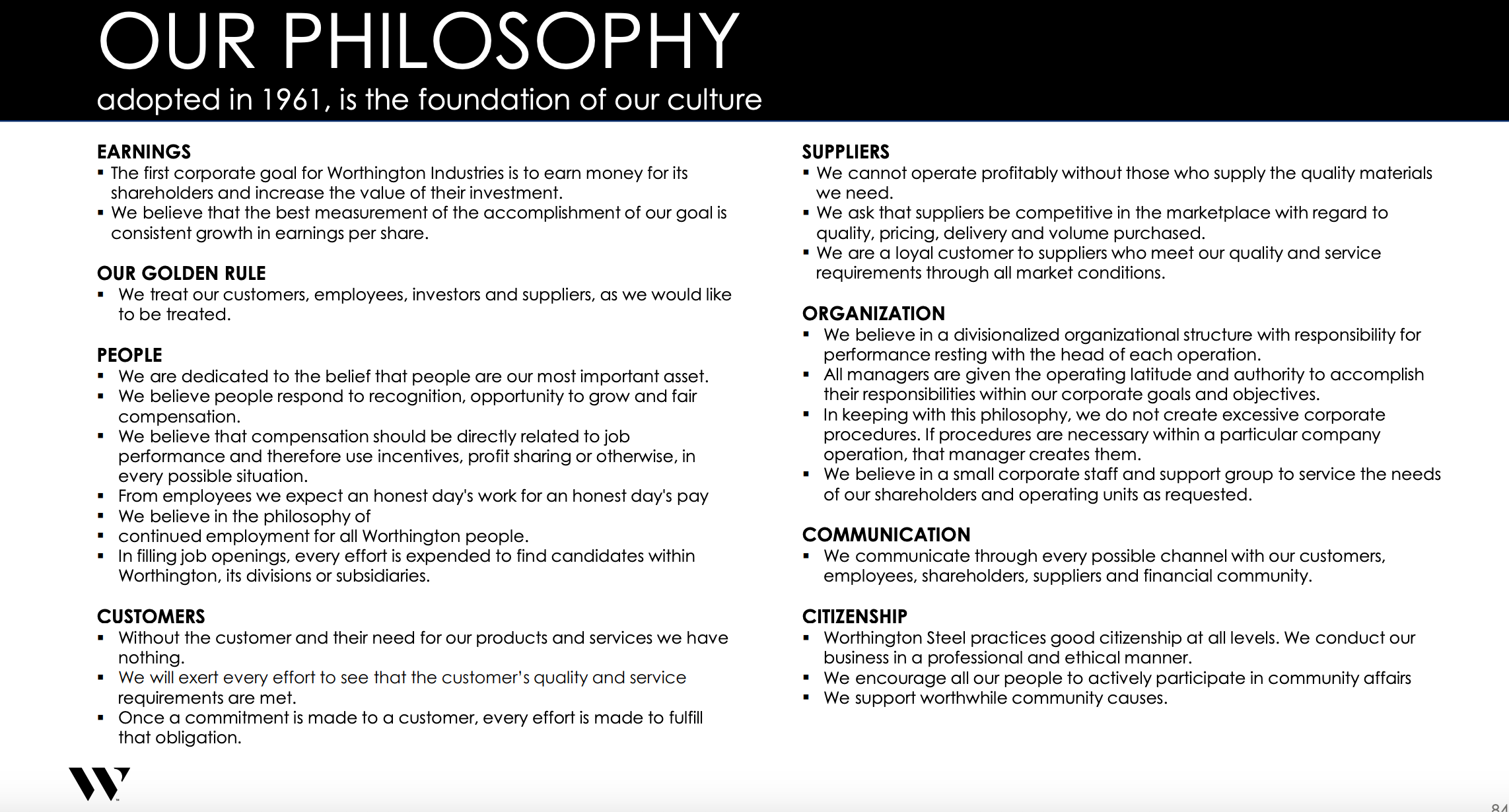

To their credit, Worthington’s IR team promptly published the transcript to the investor day. This is a small but telling indication that the company wants to engage with its shareholder base. In my book, that's a positive and consistent with the company's first corporate goal of earning money for its shareholders and increasing the value of their investment.

Moat

Worthington’s moat is narrow but durable, producing about 20% returns on invested capital (defined - appropriately - by the company as NOPAT/Average Invested Capital). Management’s goal is to increase ROIC in the coming years.

At investor day, Worthington laid out where it believes it has durable competitive advantages:

Worthington's moat is rooted in cost advantages rather than product differentiation. However, the company aims to do more product differentiation in the coming years, which might command higher NOPAT margins.

Worthington must retain and increase its wallet share with its customers for the cost advantages to persist.

As Columbia professor Bruce Greenwald writes in Competition Demystified, “For economies of scale to serve as a competitive advantage, they need to be coupled with some degree of incumbent customer captivity.”

This strategy is consistent with what Worthington laid out in the slide above. Most of their barriers to entry are related to