Flyover Stock: Worthington Industries (WOR)

An uncommon spin-off story where the opportunity is with the RemainCo

Executive summary

Forthcoming “early 2024” spin-off of steel processing business could unleash more buyback, dividend, and/or M&A activity at the RemainCo

Founding McConnell family owns 35% of the business; founder’s son remains executive chairman

Spinning-off the highly-cyclical, low-margin steel processing business leaves a capital-light, more forecastable, niche building and consumer products business with 20% adjusted EBIT margins

At Flyover Stocks, we’re looking for overlooked quality businesses with economic moats led by thoughtful stewards of shareholder capital.

Sometimes, you can find flyover stocks right under your nose. Worthington Industries’ (NYSE: WOR) headquarters in Columbus, Ohio, is about 120 miles from my house. Over the years, I must have screened for Ohio-based companies a few dozen times, but I can’t recall digging into Worthington.

I can tell you why I must have passed on it before - its primary industry is steel. Having worked on a basic materials desk from late 2011 to 2015, I remember the bust in steel prices that followed the China boom. And in any case, the steel industry isn’t abounding with economic moats. My guess is that other quality-minded investors have also passed on Worthington for this reason. Currently, the stock only has four sell-side analysts, which suggests there isn’t much institutional interest.

Three things about Worthington piqued my interest this time around.

First and foremost, the company is spinning off its low-margin, cyclical steel business (Worthington Steel/“NewCo”) and keeping a gem of a business. The “New Worthington” (“RemainCo”) will feature higher-margin, capital-light building products, consumer products, and sustainable energy operations.

Typically, the NewCo is the focus of spin-off stories, but not in this case. Here, the RemainCo is more interesting.

Second, the CEO Andy Rose is sticking with the RemainCo. Rose is the first non-family member to run Worthington and owns 1.3% of the shares. Since he joined the company as CFO in 2008, the company has retired 40% of its shares. He became CEO in 2020. More on him in a moment, but he’s a potential “outsider-type” CEO who is about to get a steadier cash flow machine.

Finally, the founding McConnell family culture and 35% ownership should continue to allow Worthington to think and act with a long-term mindset. While this doesn’t guarantee success, it provides fertile ground for it.

Over the years, Worthington has traded like a cyclical steel stock – 5 year beta of 1.30, 5-year P/S average 0.7x, etc. – which has systematically undervalued the steadier, higher margin building and consumer products businesses. That alone makes Worthington worth a look, but I think there could be even more opportunity in the years ahead.

Let’s dive into the company.

Business overview

Market cap: $3.60 billion

Enterprise value: $3.94 billion

Revenue TTM: $4.92 billion

Net debt/Adjusted EBITDA: 0.46x

Dividend yield: 1.75%

Number of analysts covering: Four

All market data as of August 18, 2023

Let’s start with the business that Worthington is spinning off. Worthington Steel (NewCo) is the company’s legacy value-added steel processing business accounting for 71% of FY 23 revenue (fiscal year ends May) and 30% of FY 23 Adjusted EBIT. It primarily serves the auto and manufacturing industries. While it seems to be one of the better steel companies out there, it’s not the type of business I want to own.

The pressure cylinders business, which forms the backbone of the RemainCo, was acquired in 1971 when Worthington bought an unprofitable operation from Lennox and made it profitable the following year. The company manufactures pressurized steel and aluminum cylinders that hold various gases, including propane, hydrogen, refrigerant, natural gas, and helium. There’s a good chance, for example, that Worthington manufactured the propane tank under your grill.

Pressure cylinders are used in the building products and consumer products industries. Worthington’s building products pressure cylinders are used in HVAC, refrigeration, commercial cooking, chemical, plumbing, and fire suppression. Worthington believes it has the largest market share in the domestic low-pressure cylinder market, and is the only US manufacturer of non-refillable DOT-39 cylinders used by HVACR technicians to carry refrigerant.

Low-pressure cylinders are used for liquified petroleum gases, such as propane and refrigerant. On the other hand, high-pressure cylinders are used for gases such as hydrogen, oxygen, and helium.

Consumer Products include cylinders of various sizes used in the tools and outdoor living markets. This group makes the exchangeable propane tanks used in barbeque grills and recreational vehicles, in addition to tanks used in camping stoves, helium balloon inflation, and handheld torches.

Finally, the Sustainable Energy Solutions segment is primarily based in Europe and sells alternative onboard fueling systems for buses, automobiles, and light-duty trucks.

Worthington includes a few consolidated and unconsolidated joint ventures, including WAVE, a 50/50 JV with Armstrong World Industries, which makes commercial and residential ceiling suspension systems. If your office has checkerboard ceiling tiles, there’s a good chance the metal framing came from WAVE. Some of these JVs, including WAVE and ClarkDietrich metal framing, will be part of the New Worthington RemainCo, under the Building Products segment. They are accounted for using the equity method.

WAVE and ClarkDietrich will be significant contributors to the RemainCo. In fiscal 2023, the two combined added $166 million to the Building Products segment profitability. Together, they sent Worthington $240 million in dividends last fiscal year. WAVE is the largest of four North American ceiling suspension systems manufacturers, and ClarkDietrich’s metal framing, building systems, and drywall products have benefitted from robust commercial construction activity in recent years.

Moat

As you might imagine, metal cylinders and tanks filled with flammable and combustible gasses are part of a tightly regulated supply chain. Worthington sells fillable and non-refillable cylinders and fills some non-refillable cylinders, such as helium tanks, in-house before shipping. The entire chain, from the cylinder manufacturing to the filling process, to the delivery and exchange, requires compliance and tight controls. Trust and reliability also matter as the liability of a faulty tank could cause reputational damage for various parties.

In some instances, the cost of the tank is small (but mission-critical) relative to the ultimate service provided to the end customer. A propane exchange company, for example, may have to replace a tank once every decade and wants to focus on selling and refilling the propane at an attractive margin. It does not want to worry about the tank’s durability or reliability.

The average Building Products and Consumer Products revenue per unit sold is approximately $50 and $9, respectively. These are not high-priced items, so Worthington needs to have high manufacturing efficiency and a lot of volume to turn a profit.

The US Department of Transportation is the governing body that regulates portable cylinders. Each tank has a stamped date for recertification, typically between 5 and 12 years from manufacture, which ensures that the tanks are still suitable for carrying gases.

Shipping stacks of empty and gas-filled cylinders is a low value-to-weight proposition and a barrier to entry for a would-be competitor. Put differently, it’s expensive to ship metal cylinders filled with gas over long distances. Indeed, a truck driver carrying more than 1,001 pounds of compressed gas must have a hazmat (hazardous materials) license and a CDL. Transportation costs can add up quickly the further out the destination.

These factors should limit competition from imports, but as we’ll discuss in risks, that doesn’t mean imports can’t or won’t be a factor at different parts of the cycle.

New Worthington’s product lines should remain relevant over the next decade. Notably, the pressure cylinders business remained profitable during the financial crisis, and gross margins have consistently ranged between 20% and 25%. Much will depend on how much building – residential, commercial, and industrial – happens in North America in that time frame. You can probably stop reading if you don’t expect strong infrastructure spending in North America over the next decade.

The company is also innovating in relatively unsophisticated markets to maintain and grow its relevance with customers. One example is the SmartLid, a plastic cap with wireless sensors placed on top of tanks and saves fuel distributors time by knowing exactly how much gas is in a tank before they arrive.

While the RemainCo is far from a wide moat business, I think it does have a narrow moat supported by cost advantages related to the sourcing of the raw materials (Worthington is one of the largest buyers of steel in North America after the automakers), manufacturing know-how, and low-cost transportation.

In the coming weeks or months, we will get more granular data to measure and track the RemainCo moat and moat trend once the spin is completed, but in the meantime, keep an eye on revenue per unit sold and margins.

Stewardship

Worthington was founded in 1955 by John H. McConnell, a business leader I enjoyed reading about while doing this research. Born in West Virginia, McConnell grew up during the Great Depression, served in the Navy on the USS Saratoga during WWII, worked in steel mills, used the GI Bill to get a business degree from Michigan State University, and took $600 that he borrowed against his car to buy a roll of steel to start Worthington.

John H. emphasized servant leadership, and his Golden Rule approach to doing business remains a core tenet of the company’s culture today. Later in life, McConnell helped bring the first professional sports team – the NHL’s Blue Jackets – to Columbus. You can learn more about him here, and I would encourage you to do so after reading this.

His son, John P., was CEO from 1993 to 2020 and is Executive Chairman. He owns 35% of Worthington, as of the last proxy. John P. started at Worthington as a general laborer and learned the business from the ground up. In January, he announced he would step down from the board, but in June reversed his decision and will remain on the board through the spin-off with an undetermined exit.

Why does the family history matter? An integrity-based culture like the one John H. started and a company in which the founding family retains significant ownership stake can be a powerful force for value creation. Companies like this can financially and culturally endure near-term pain because of employee and ownership buy-in and delay gratification in pursuit of long-term growth.

While Andy Rose is not a member of the McConnell family, there are family links. His grandfather and John H. went to high school together in West Virginia. They even played football together, served on the school’s student council together, and remained friends afterward. But before you raise an eyebrow at the nepotism risk, know that Rose has the experience and background for the job. Prior to joining Worthington, the bulk of his career was in private equity, specializing in capital allocation, acquisitions, and financing.

Since joining the Worthington ranks in 2008 as CFO, the company has pivoted to being more thoughtful about capital allocation. One illustration of this is Worthington’s aggressive buyback push over the last 15 years. Considering the volatility and low forecastability of the steel processing business, regularly retiring stock while paying rising dividends is no small feat. As such, the New Worthington business model will provide Rose with more reliable cash flow to create shareholder value through prudent capital allocation.

On the separation call, Rose said: “Why are we doing this and why now? First, our management team and board are laser focused on shareholder value, and it has become clear that we have two very distinct businesses that should be valued differently and will benefit from their own strategic focus and capital allocation priorities.”

Indeed, the capital allocation priorities for a steel processing business are materially different from that of a building and consumer products business. The fact Rose was able to reduce the share count by 40% over 15 years with the burdens of the steel business’s capital intensity and cyclicality bodes well for what may lay ahead with New Worthington.

The company has a long history of focusing on shareholder value creation, having paid a dividend every year since it went public in 1968, and spinning off operations as needed. Management financial incentives include an Economic Value Added (EVA) metric that measures how much value the company created above its cost of capital.

Notably, the company paid an additional quarterly dividend in December 2012 ahead of the 2013 tax law change that increased the tax on dividends. To me, this is evidence that they are regularly considering shareholders. Separately, it’s a positive when a company presents and archives investor communications transparently on its investor relations page, which Worthington does. It provides archived earnings transcripts and presentations - something most large-cap companies with large investor relations teams do not do.

Considering the cyclicality, capital intensity, and low forecastability of the steel business, Worthington’s stock has significantly outperformed its industry and kept up with the general market over extended periods.

Rose has said he’s done approximately 60 deals in his career, including about 20 at Worthington. In more than one source, Rose said he follows the Warren Buffett quote to “be greedy when others are fearful” when it comes to acquisitions. A Buffett-quoting CEO can be a yellow flag, but the mentions didn’t strike me as marketing, as they were told to a local business journal and a group of university students. He’s also on record saying he’s a passionate investor, which is what got him into private equity in the first place.

As an aside, Worthington made an early $2.5 million investment in Nikola that gave them a 10% equity stake in the business. During the SPAC mania, the investment was worth over $1 billion. Eventually, Worthington was able to exit with a gain of over $600 million. After paying taxes, $20 million went to community endowment, and $30 million went to employees (approximately $3,500 per employee based on 2022 employee count), which exhibits the company’s approach to sharing its success with key stakeholders.

Risks

Despite the low value-to-weight transportation advantage, foreign producers will still try to enter the North American pressure cylinders market. There have been instances of alleged dumping by foreign producers at various times, and Worthington has successfully defended its position in national and international courts.

The RemainCo businesses are firmly legacy moats, with limited reinvestment opportunities in them. Future growth will rely on management execution, innovation, and smart M&A activity.

Worthington’s two big JVs – WAVE and ClarkDietrich – will be material contributors to the RemainCo’s profitability. Any disruption in either of those businesses could dramatically reduce available cash flow for Rose to employ in the RemainCo.

Post spin-off, the RemainCo may have less bargaining power with raw material producers, which could impact margins if Worthington is unable to pass on added costs.

Valuation

Legacy Worthington would fall into the “too hard” pile for me, mainly because of the steel business. To be sure, New Worthington is approaching the borderline of complexity, as well, given the dependence on JVs and the resulting adjustments that are made to operating profit to understand the underlying economics of the business. But we can nevertheless take a shot at valuing it and sizing up the opportunity post-spin.

The fact that we still need full financials for the RemainCo limits the ability to do a full DCF model, but Worthington has provided some key data points for us to work with.

Legacy Worthington has traditionally traded with a price-to-sales (P/S) multiple reflective of its steel processing business – i.e. low profit margin, moderate growth, and a high cost of equity.

Over the last five years, Worthington traded with an average P/S of 0.7x, according to Morningstar.

Suppose we apply price-to-sales ratios between 0.5x and 0.7x on Worthington’s steel processing business revenue over the last twelve months. In that case, we will arrive at an implied Worthington Steel market cap between $1.75 and $2.5 billion.

Subtracting those amounts from the current market cap of $3.6 billion, leaves the implied RemainCo market cap range between $1.1 and $1.9 billion.

In the fiscal year ended May 2023, RemainCo generated $1.42 billion in revenue and, assuming Worthington splits the debt and interest expense equally between the NewCo and RemainCo, and pays a 25% tax rate at RemainCo, it would work out to approximately $203 million in adjusted net income for the remaining business.

If we assume the market places a 0.5x P/S on the steel business after the spin, that implies that today the RemainCo is trading with an implied ~10x price-to-adjusted net income basis. We’re looking at ~11x if we subtract restructuring and separation costs from the adjusted earnings figure.

Rose has mentioned that he is aiming for 7-10% revenue growth, which is a buildup of 2-3% GDP growth + 2% transformation + 2% innovation/new products growth + 2% acquired growth. Holding margins flat and a continued buyback pace of 3-4% per year implies 10-14% EPS growth. If RemainCo can achieve this, today’s implied valuation looks attractive.

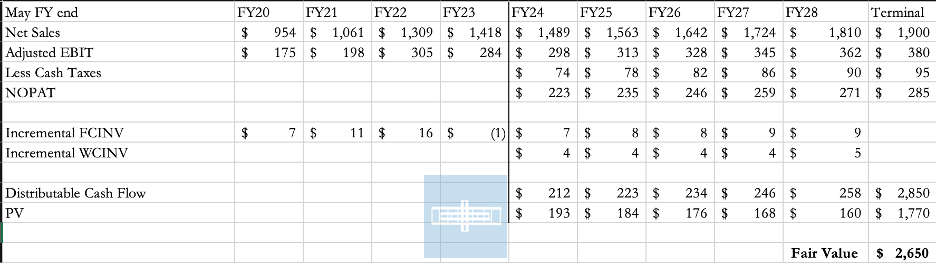

I separately ran a simplified DCF with the information available on the RemainCo. I assumed 5% sales growth for the next five years, adjusted EBIT margins of 20%, 25% book tax rate (could be lower in cash terms), 10% incremental fixed capital investment rate, 5% incremental working capital investment rate, a 10% cost of capital. Terminal value assumes steady-state NOPAT/Cost of Capital.

That scenario showed the fair enterprise value to be $2.65 billion. Assuming RemainCo gets half of the Q4 2023 net debt ($119 million) and half the unfunded pension liability (~$12 million), it would get you to a fair equity value of about $2.5 billion. Again, you may want to un-adjust the EBIT, but the RemainCo looks attractive here, too.

These are back-of-the-envelope calculations, but they’re a good starting point.

In my experience, the market can serially undervalue good acquirers, as analysts typically do not include M&A in their models until the deals are announced. From what I’ve read and heard about Rose, he seems to “get it” from a capital allocation perspective. If Rose is able to execute on his plan for 7% to 10% revenue growth, expands margins, and buys back stock at 3% to 4% per year, the above estimates will prove conservative, indeed.

Bottom line

While Worthington will likely be one of the more complex businesses we look into at Flyover Stocks, it’s an excellent example of the type of opportunity I’m looking for – an overlooked quality company led by thoughtful allocators of shareholder capital. If you’re confident in North American re-shoring and capital investment, I think Worthington is worth a look, before and after the split in early 2024.

At the time of publication, Todd and/or his immediate family did not own shares or have a financial interest in any company mentioned in this article.

Disclaimer:

This material is published by W8 Group, LLC and is for informational, entertainment, and educational purposes only and is not financial advice or a solicitation to deal in any of the securities mentioned. All investments carry risks, including the risk of losing all your investment. Investors should carefully consider the risks involved before making any investment decision. Be sure to do your own due diligence before making an investment of any kind.

At time of publication, the author or his family may have an interest in the securities mentioned or discussed. Any ownership of this kind will be disclosed at the time of publication, but may not be updated if ownership of a particular security changes after publication.

This newsletter does not provide buy or sell recommendations and articles should not be interpreted this way.

Information presented may be sourced from third parties and public filings. Any links to these sources are included for convenience only and are not endorsements, sponsorships, or recommendations of any opinions expressed or services offered by those third parties.

Thanks for the wonderful post. I ask this question as a *general* question, as I don't want you to feel the pressure to prescribe specific buy/sell advice on a company like Worthington: when you find an interesting spinoff at an attractive valuation, how do you think about when to buy? For example, in this case -- you're more attracted to the RemainCo than LegacyCo, so do you wait until the spinoff to concentrate your investment into RemainCo, or do you start a position now considering that more folks may fine Worthington and eliminate the discount?

In Greenblatt's book, it seems he often would wait for the split as splits can generate a depression in price for a variety of reasons, but of course there's no one hard rule and these things should be taken on a case by case basis. I'd just be curious how you think about that question!