The Omar Vizquel Portfolio: How "Optimizing" Kills Your Winners

New data from Morningstar shows that active managers’ best move might be to do nothing.

“You just got lesson number one: Don’t think. It can only hurt the ball club.” - Bull Durham

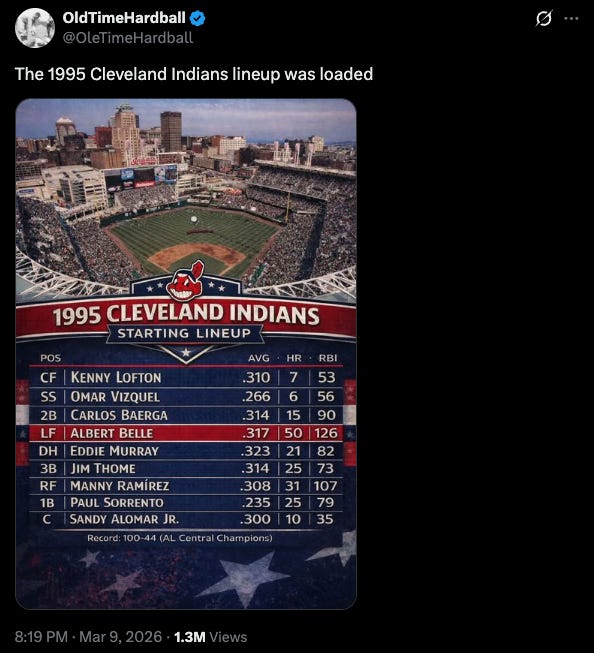

The 1995 Cleveland Indians (now the Cleveland Guardians) baseball team is regularly listed as one of the top 50 of all time. They had 100 wins and just 44 losses on the season. They led the majors in runs, hits, home runs, and batting average - just about every major offensive category.

In most years, they would have won the World Series, but they ran into the equally impressive 1995 Atlanta Braves who beat them four games to two in the finale.

The dominant 1995 Indians starting lineup recently made its rounds on Twitter and caused a lot of debate.

Most of the critique was regarding the placement of Omar Vizquel, better known for his glove than his bat, at second in the lineup. (For the uninitiated, the second hitter in the lineup gets more chances to hit each game and plays a strategically important role ahead of the “power hitters” in the third through fifth spots.)

“Moneyball” has since been introduced to Major League Baseball and there’s no way Vizquel would hit second in today’s game. He’d more likely hit eighth or ninth - and may not have even played at all despite his excellent defensive skills.

Today, baseball is fully optimized. Every pitch, every movement is charted, analyzed, and studied. Probabilities are determined to drive decisions. “Gut” feelings from managers are insufficient if the probabilities suggest the alternative.

And yet…this team won 70% of its games.

“Well,” you could argue, “That’s only because the other teams in the league were also unoptimized.”

That might count for a few wins, but even if the league were more optimized, this lineup would have still produced top quartile results.

That’s because it’s hard to be average when you are stacked with “right-tail” talent - that is, talent well above the population average. You could have organized Cleveland’s lineup a dozen different ways and they still would have done well.

This got me thinking about portfolio management. Are active portfolio managers over-optimizing their portfolios and missing the point, which is to own and hold what they believe to be “right-tail” stocks?

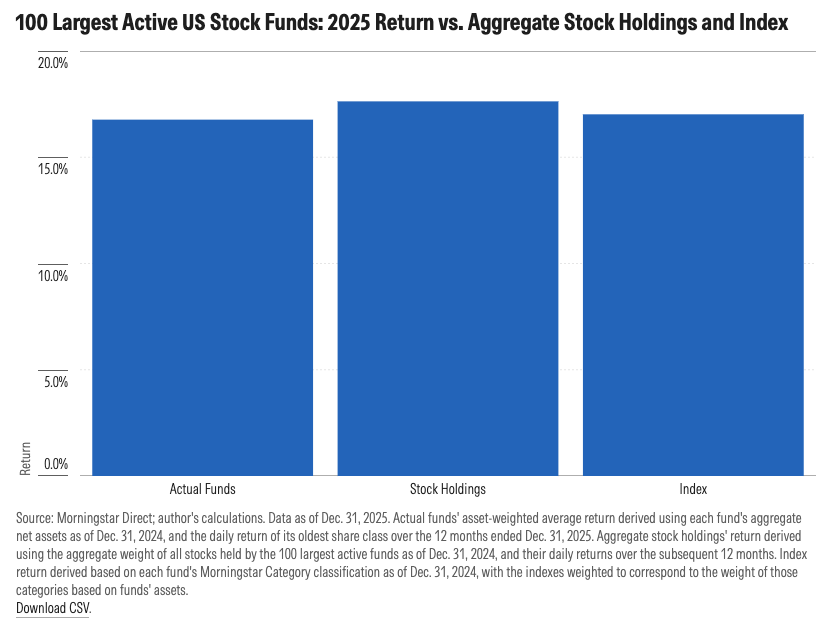

Jeff Ptak, Managing Director of Morningstar Research, recently studied the 100 largest active U.S. stock funds. He compared their actual 2025 performance against a hypothetical "Do-Nothing" portfolio, which took the funds' exact holdings from the start of the year and simply froze them (no buying, no selling) for the next 12 months.

What he found was that the funds’ stock picks beat the market, but their portfolios did not.

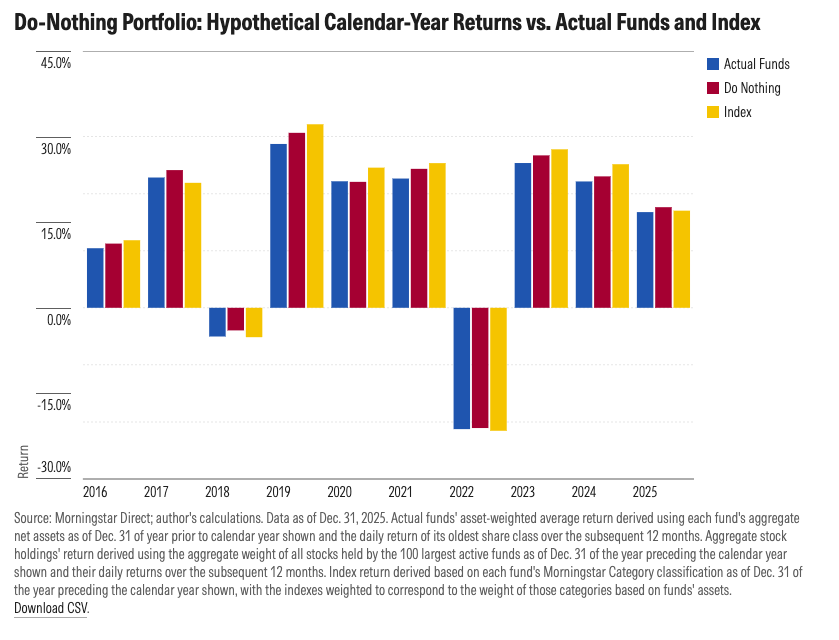

Ptak took this even further, testing the hypothesis over a longer time period, and the result was much the same. In nine of the last 10 years, the “do nothing” portfolios did better than the actual fund results.

Put differently, portfolio managers as a group traded their way out of better performance, presumably to optimize their portfolios.

Just as is the case with Major League Baseball, there are good reasons for portfolio managers to optimize and consider risk-adjusted probabilities and payoffs. There are also times where selling is absolutely the correct decision, even if the outcome turns out to be suboptimal.

But we can also trade not because the business changed, but because the portfolio’s lineup looked messy on a spreadsheet. We might bench our home run hitters just as they’re getting into a rhythm, usually to satisfy some volatility constraint or a rebalancing rule that has nothing to do with the company's actual compounding power.

The right-tail of the stock universe is, by definition, limited. And as Henry Bessembinder’s data shows, only a fraction of stocks account for the majority of the stock market’s returns.

If we believe our process increases the likelihood that we are identifying right-tail stocks, then, we should also err on the side of not selling or trimming them in order to “optimize” the portfolio.

Given the way the math works, one right-tail stock held patiently can make up for a lot of sub-optimal decisions.

Sometimes we need to get out of the way and let the team play. Or as my kids would say, “Let them cook.”

Stay patient, stay focused.

Todd

Todd Wenning is the founder of KNA Capital Management, LLC, an Ohio-registered investment advisor. KNA Capital Management manages a concentrated equity strategy and provides other investment-related services.

At the time of publication, the author, his immediate family, and/or KNA Capital Management, LLC or its clients own shares of Morningstar.

This profile is for informational purposes only and does not constitute personalized investment advice or a recommendation to buy or sell any security.

Please see important disclaimers.