Stock Duration: What It is and Why It Matters

What bond math can teach you about your stock portfolio

If you don’t understand stock duration, you may have hidden risks in your portfolio.

Investors, analysts, and commentators will often throw around the phrase “duration” as it relates to stocks, but rarely do people explain what they mean by it.

Duration is a term more commonly used in the fixed income world. A bond’s duration is a good approximation for how much the bond’s price will change given a +/- 1% change in interest rates.

For example, a bond with a duration of 8 years should increase in value by 8% if interest rates decline by 1%, and vice versa.

But what exactly is duration?

In simple terms, duration measures how dependent an asset’s value is on distant future cash flows.

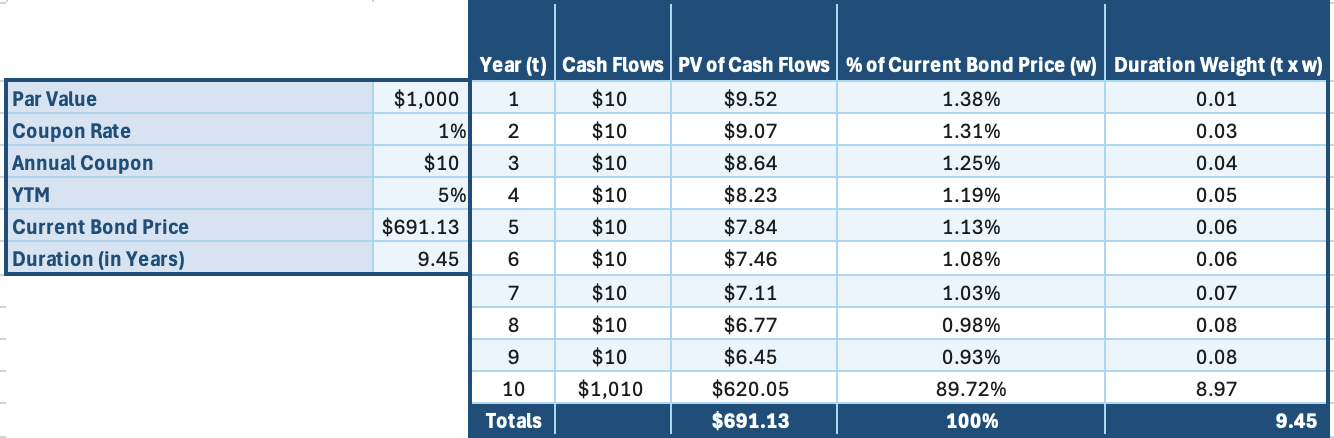

To keep it simple to start, let’s say we have a 1% annual coupon ten-year bond with a $1,000 par value. That means we collect $10 per year, each year, until maturity. At maturity, we get our final $10 coupon payment and the $1,000 par value back.

If the yield to maturity (i.e. the discount rate) is 5%, then the bond’s price is $691.13 - the sum of future cash flows discounted back to the present.

Pay attention to the contribution (% of Current Bond Price column) of each cash flow to the price.

Fully 89.7% of the bond’s price comes from the final year (Year 10) cash flow because it includes the return of the $1,000 par value. This $1,000 payment dwarfs the $10 coupon payments received each year and is thus the major driver of price.

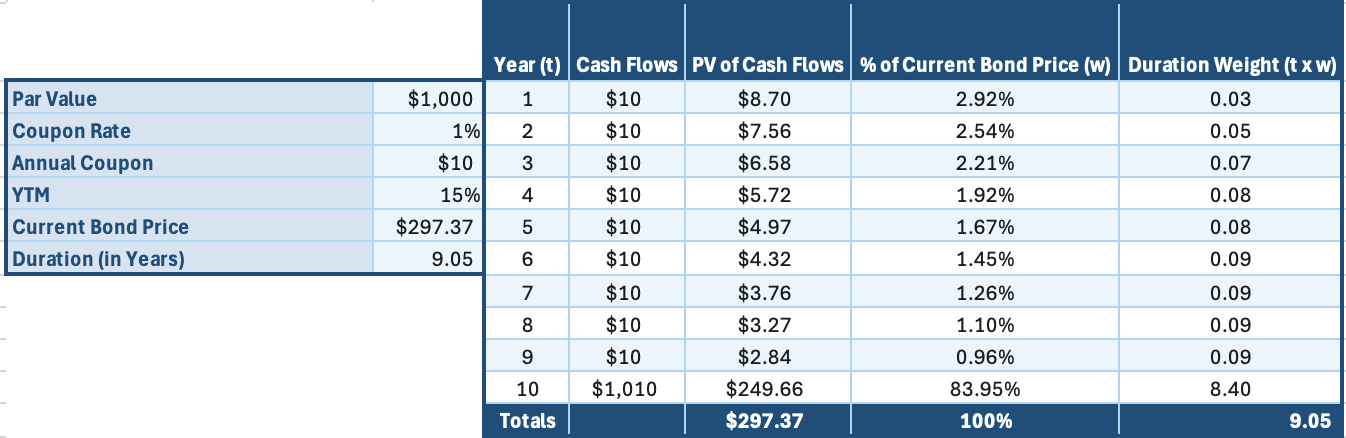

Watch what happens when the yield to maturity spikes to 15% from 5% in the previous example.

Not only does the bond price decline by 57% to $297.37, but the contribution of the big Year 10 cash flow also declined from 89.7% to 84%. The nearer-term cash flows become relatively more important to the bond’s price.

In other words, the cost of waiting for that distant cash flow just went up - by a lot - and is therefore worth less to me relative to the nearer-term cash flows.

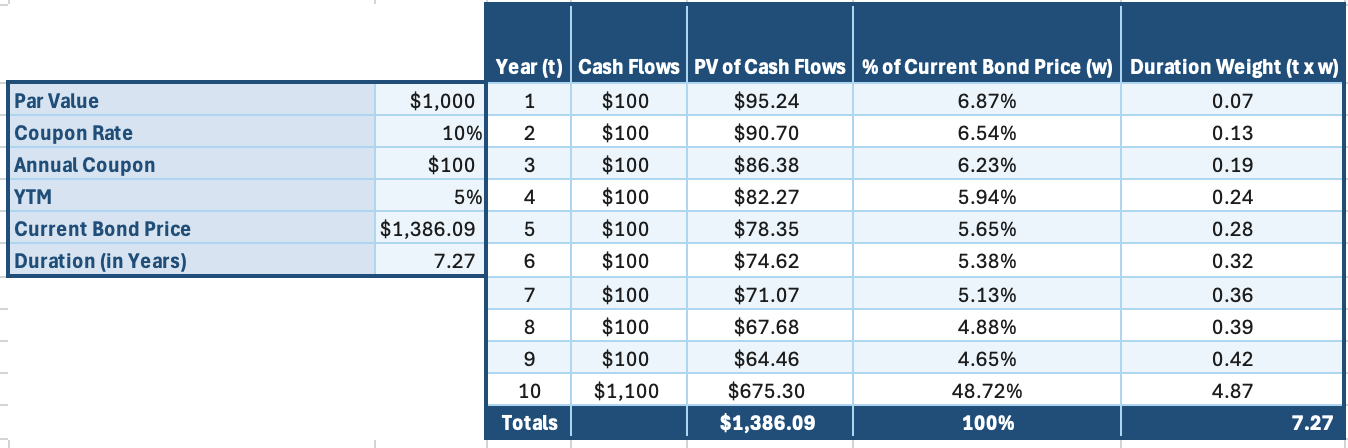

Contrast the above bond with a bond that pays a 10% coupon - $100 per year - under the same scenario.

Here, because the 10% annual coupons are more substantial, they carry more of the weight in the current bond price versus the 1% coupons above. Put differently, you get paid more while you wait.

In the 5% yield to maturity scenario, the Year 10 cash flow only accounts for 48.7% of the current value (versus 89.7% for the 1% coupon bond).

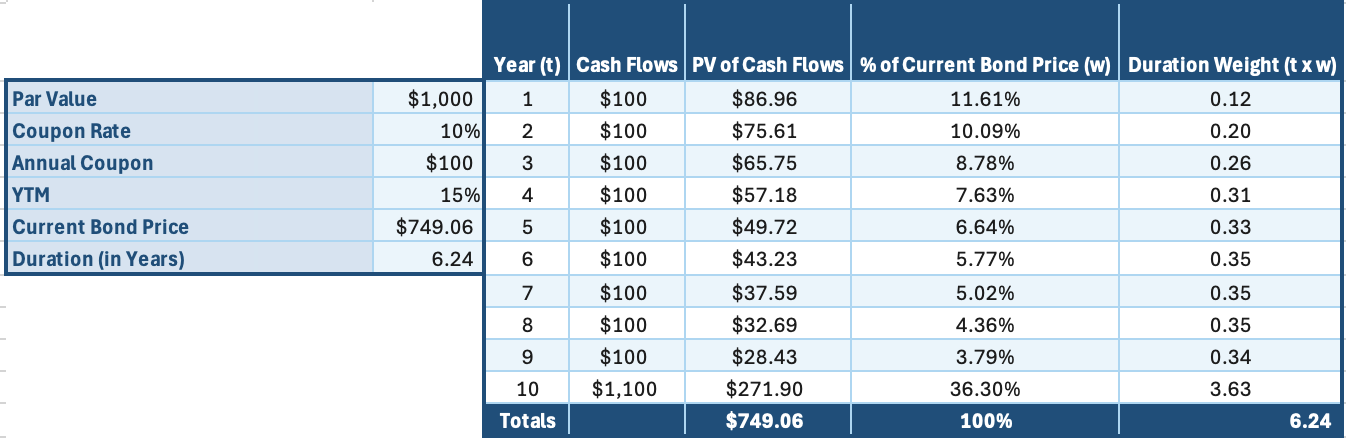

As a result, when the yield to maturity jumps to 15%, the 10% coupon bond still falls in price, but declines 46% instead of 57%.

A similar dynamic happens with stocks, even though the cash flows aren’t spelled out and there isn’t a maturity date.

The more a stock’s valuation depends on long-dated assumptions and terminal value, the more sensitive it becomes to changes in interest rates or risk perception.

This puts growth stocks in a particularly vulnerable position when interest rates rise sharply (as we saw in 2022) and/or risk premiums increase.

A company trading at 40x earnings may still be a bargain in the long-run, but it’s more likely to be a bumpy ride unless conditions remain favorable. That’s because so much is riding on the cash flows the company is expected to earn a decade or more from now. In other words, a low free-cash-flow yield stock is a long-duration instrument, like the 1% coupon bond above.

A stock with a higher starting free cash flow yield, on the other hand, is more like the 10% coupon bond. It’s not immune to changes in the risk environment, but it’s less sensitive because more of the stock’s current value is coming from nearer-term cash flows.

If your portfolio owns a lot of high-growth, high-P/E, or low free cash flow yield stocks, then you may have hidden duration risk. A big part of prudent portfolio management is risk management, so it’s important to be aware of not just company-specific risks, but how those companies, as a portfolio, respond to shifts in rates or risk appetite.

Investors can reduce duration risk by balancing long-duration holdings with companies that generate stronger cash flows today.

Of course, stocks are not bonds. The cash flows are not known up front. A great company can earn its high current multiple through better-than-expected operational performance, and a stock with a high free cash flow yield can reflect deteriorating business quality, so lower duration does not automatically mean lower total risk.

The first step in better risk management is knowing what risks are embedded in your portfolio. Duration risk is one of those risks that are less obvious, especially when markets are rising and the risks feel abstract. Remember that the farther your portfolio’s cash flows sit in the future, the more sensitive it becomes to changes in the present.

Stay patient, stay focused.

Todd

Todd Wenning is the President & CIO of KNA Capital Management, LLC, an Ohio-registered investment advisor that manages a concentrated equity strategy and provides other investment-related services.

At the time of publication, the author, his immediate family, and/or KNA Capital Management, LLC or its clients do not have positions in any company mentioned.

Please see important disclaimers.

Excellent use of the tables to illustrate duration and explain why it is important.