Rethinking the Too Hard Pile; Earnings Updates on MEDP and YETI

How a Sherlock Holmes story can help us better allocate our mental capital between apparent simple and complex ideas.

"As a rule," said Holmes, "the more bizarre a thing is the less mysterious it proves to be. It is your commonplace, featureless crimes which are really puzzling, just as a commonplace face is the most difficult to identify. But I must be prompt over this matter."

"What are you going to do, then?" I asked.

"To smoke," he answered. "It is quite a three-pipe problem, and I beg that you won't speak to me for fifty minutes."

-Sherlock Holmes, “The Red-headed League”

In the Sherlock Holmes story, “The Red-Headed League,” Holmes is presented with what appears to be a prank on a gullible and credulous pawnbroker named Jabez Wilson.

After gaining entry into the mysterious Red-Headed League, a secret society for men with extremely red hair, Wilson was paid a handsome sum to visit an office four hours a day to copy the Encyclopedia Britannica by hand. Eight weeks later, the office was vacant and there was no trace of the league.

Upon hearing Wilson’s story, Holmes and Dr. Watson break out into uncharacteristic laughter.

After a few more questions, however, Holmes realized that what initially appeared to be a simple joke that ran its course was actually much more sinister.

As Wilson departs, Holmes asked Watson to give him fifty minutes alone - time to smoke three pipes - to think deeply about the matter. He needed to extract the complexity from the clarity.

If you’re managing a portfolio, there’s a good chance that at any given time you have at least one “three-pipe problem” on your hands - a stock that takes up a large amount of mental capital in search of a solution.

The problem isn’t that we’re thinking deeply about a stock, but that we can be drawn into the wrong one. Our curiosity is naturally attracted to complex companies and industries where there are endless threads to pull.

My fellow Munger and Buffett followers might interject here - “That’s what the ‘too hard pile is for.’”

Maybe. But I’ve often found, as the introductory quote suggests, that the correct thesis around complex or dynamic businesses tends to be quite simple.

Netflix operates in a complex and dynamic environment, which fueled a lot of the debate (and stock price volatility) over the last decade. But in the end the only question that mattered was whether Netflix would be the dominant video streaming service. That would lead to pricing power, lower subscriber churn, and operating leverage.

One of the reasons that retail investors sometimes catch onto big winners is they bring simple a simple thesis to a complex business and hold on. Professionals, on the other hand, can get bogged down in the details and overthink the thesis.

If you can get to the heart of the matter with a complex business, there’s opportunity to be found in the noise while most investors debate peripheral points.

On the other hand, as was the case with The Red-Headed League, the simplest narratives can be much more complex under the surface.

Indeed, this is the genesis of a quality trap, whereby returns suffer the double-whammy of slowing or declining earnings along with premium multiples becoming pedestrian multiples.

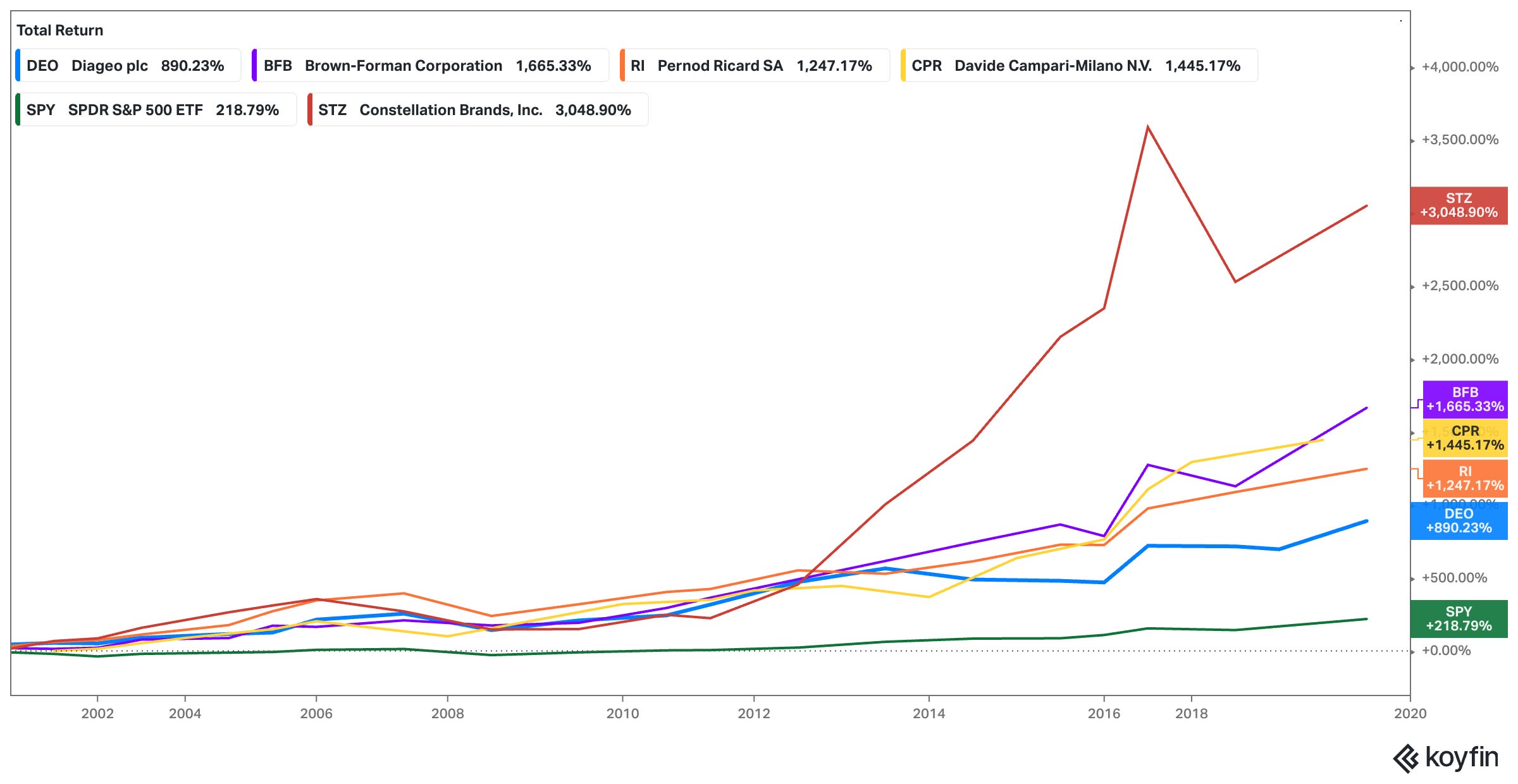

The alcoholic beverage sector today is a perfect example of this dynamic. In the 20 years leading up to the start of COVID quarantines in the U.S. and Europe, you could have thrown darts at a list of global liquor companies and crushed the S&P 500.

Liquor is relatively easy to understand and the companies’ brand- and distribution-based economic moats were clear. Liquor was recession resistant, share price volatility was low, and alongside steady growth, investors bid the stock multiples higher.

This virtuous equation didn’t go unnoticed by competitors and capital providers who wanted a piece of the pie. Celebrities launched brands and sold them, in some cases, for billions of dollars. Craft distilleries popped up across the country at a torrid pace.

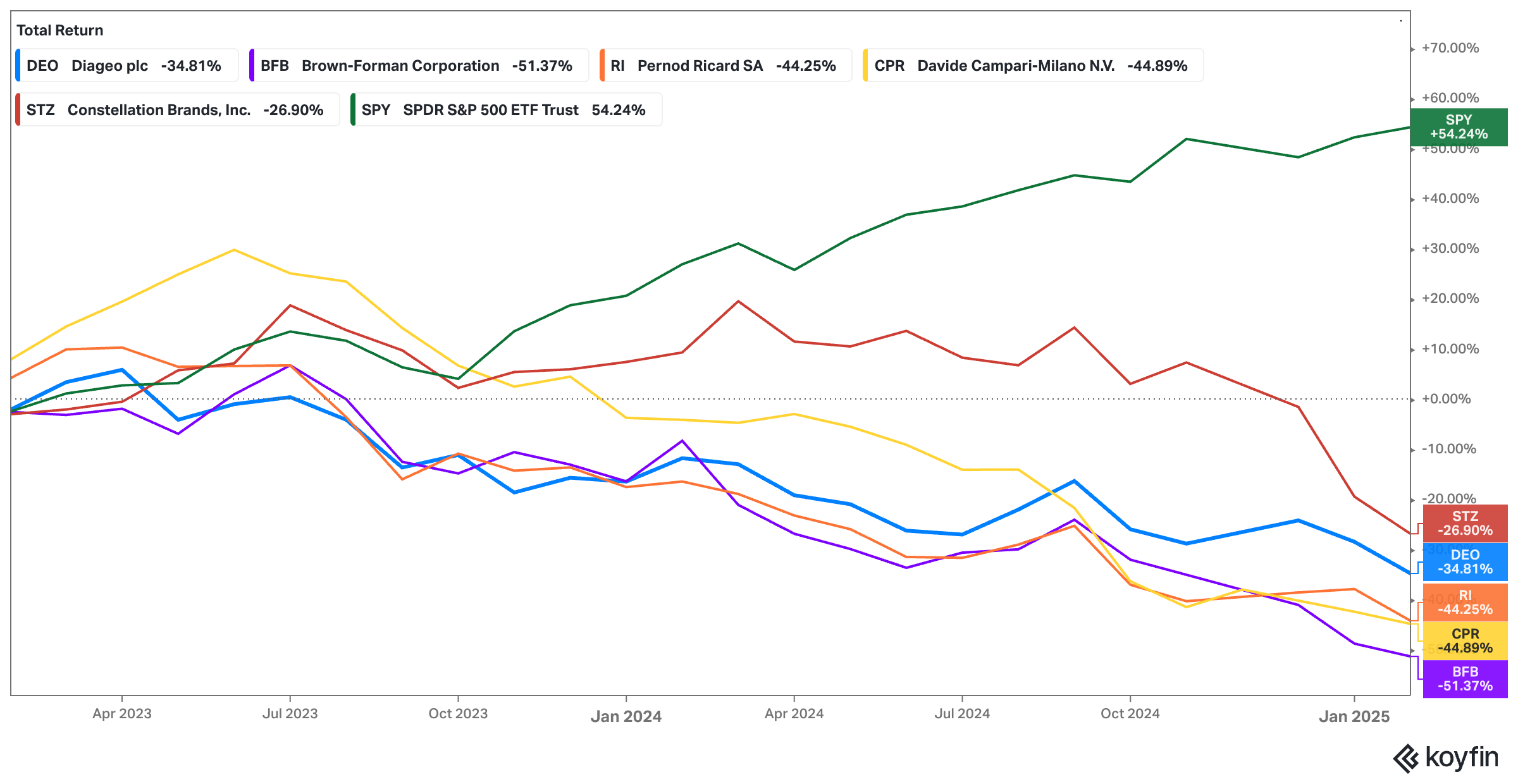

While supply flooded the market, the post-COVID surprise was that after bumper liquor sales during quarantine, a cultural backlash against alcohol consumption was growing.

Gen X and Millennials are getting older and paying more attention to their health and Gen Z demand has not filled in the demand gap left by the older generations. Social media has been abuzz with anti-alcohol messaging and GLP-1s have been shown to reduce alcohol consumption.

Consequently, the liquor stocks have struggled mightily in the last three years with slowing growth and shrinking multiples.

A few years ago, liquor stocks seemed to as close to a “buy and forget” category as you can get, but that assumption has been ripped to shreds.

Our mental capital, it turns out, should have been spent digging into the complex trends building underneath the simple investment narrative.

This passage from Sherlock Holmes is a good reminder that an investment case that seems too simple to be true probably is and that complex cases might have simple answers.

How we allocate our mental capital will impact our results, so it’s important to think twice about what we toss into the “too hard pile” and what we keep on our desks.

Paid subscribers, your content continues below.

The next Flyover Stocks company profile will be published next week. Be sure to subscribe below to stay up-to-date. Paid subscribers get the full report, which includes moat, management, and valuation analysis.

You can view previous company profiles here.

Todd Wenning is the founder of KNA Capital Management, LLC, an Ohio-registered investment advisor that manages a concentrated equity strategy and provides other investment-related services.

At the time of publication, Todd, his immediate family, KNA Capital Management, LLC and/or its clients own shares of Brown-Forman, Medpace, and Yeti Holdings.

Please see important disclaimers.