Flyover Stock: Installed Building Products (IBP)

Another Ohio company flying under most investors' radars that's producing great fundamental - and market - results.

Executive summary:

Over 20 years of steady acquisitions and organic growth, IBP has increased its share of the residential construction insulation market from 5% to 30%.

Chairman and CEO Jeff Edwards is a second-generation owner of the business and controls 16% of the shares. Buybacks are opportunistic and the introduction of a special dividend suggest thoughtful capital allocation.

Insulation is a “nuisance” product in the homebuilding process and IBP has become a mission-critical partner to regional and national homebuilders.

I dream of better insulation every winter. Our house is almost 90 years old and has plaster walls, which don’t provide much protection from icy blasts.

As I write this, the wind chill in Cincinnati is -6 degrees Fahrenheit (-21 degrees Celsius). Insulation is front of mind.

One thing is for sure – I’m not alone in my lack of proper insulation. According to the North American Insulation Manufacturers Association, over 90% of U.S. buildings are under-insulated based on the 2006 International Energy Conservation Code’s prescribed efficiency standards. While that’s like a trade organization of barbers telling you to get a haircut, I think that’s directionally true.

With that backdrop, I’d like to introduce today’s Flyover Stock company: Installed Building Products (IBP), a Columbus, Ohio-based installer and distributor of building products focused on insulation.

IBP traces its roots back to Edwards Insulation, a one-store insulation business created by Peter Edwards in 1977. The company started its current journey when Peter’s son, Jeff, joined the family business in 1994 and started rolling up small insulation installers around the country. Jeff, who is the chairman and CEO, as of the last proxy owned or controlled over 16% of shares. He’s overseen more than 100 acquisitions during his time at IBP.

Through acquisitions and organic growth, IBP has increased its market share of the U.S. residential insulation installation from 5% in 2005 to a 30% share today, making it the second-largest player in the space. Together with TopBuild (~40% share), the two companies account for over two-thirds of residential insulation installed in the U.S.

Insulation is an attractive niche. In a newspaper interview, Edwards referred to insulation as a “nuisance product” that homebuilders don’t want to deal with on their own. You can appreciate this observation if you’ve ever worked with fiberglass insulation and discovered invisible fiberglass splinters in your hands.

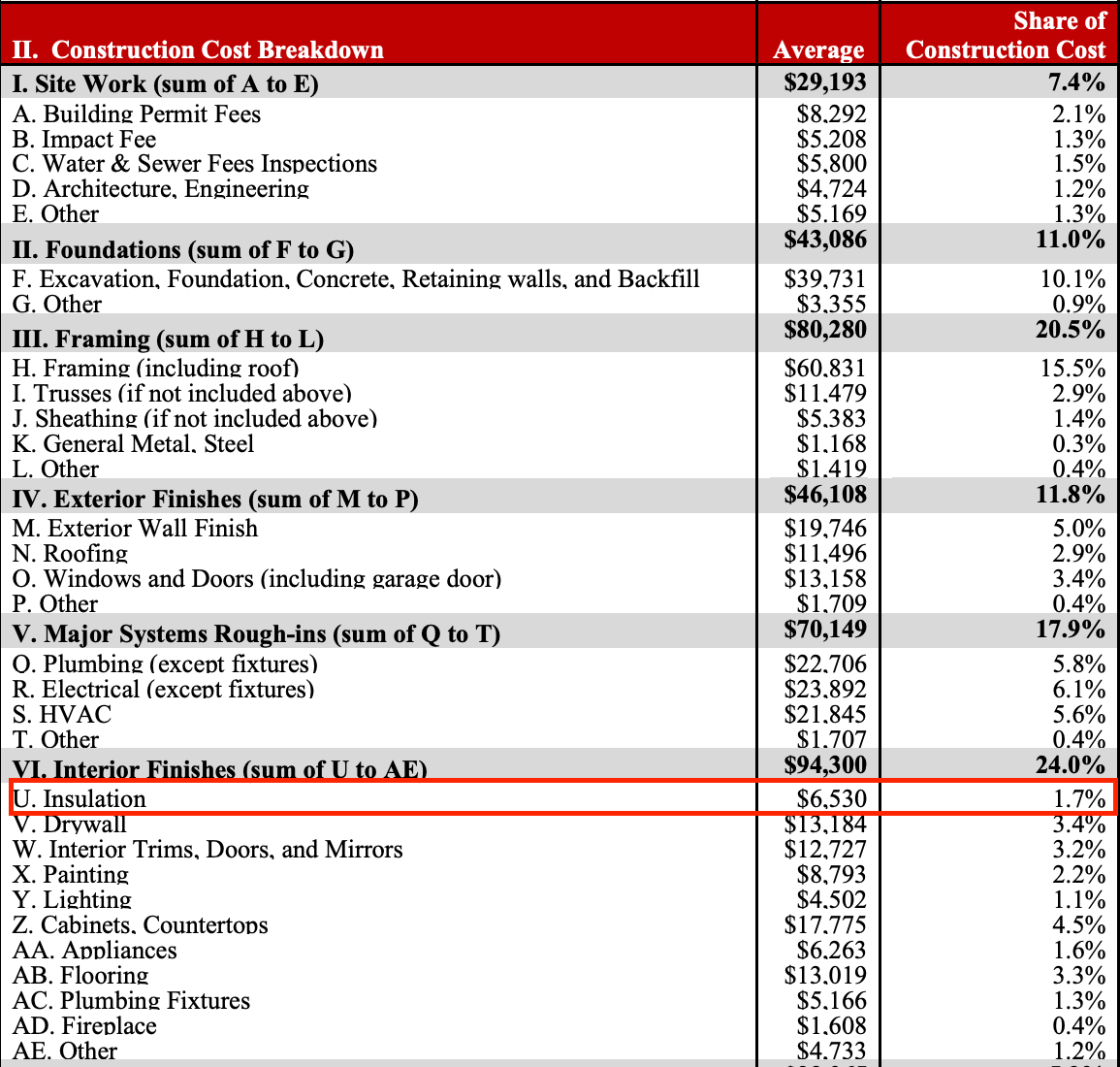

Further, according to the National Association of Home Builders’ 2022 survey, insulation in a newly constructed single-family home costs $6,530 on average. By this measure, the insulation is just 1.7% of the home’s total construction costs. That’s less than painting and offers a modest return on investment via regular heating and cooling cost savings.

Insulation is a relatively small expense but is mission-critical to the construction process. Housing codes (and common sense) require insulation in a house, and the difference between the best and worst options does not have a material impact on the overall cost of the house.

As we’ll discuss in a moment, there are other tailwinds behind insulation demand in the coming decade and beyond.

I’m intrigued by products and services that are mission-critical components yet account for a fraction of the overall cost, as customers are unlikely to switch providers due to price alone. Why risk a change? The purchasing manager does not want to report failure or project delay because they tried to save a few pennies on a minor component. This dynamic gives suppliers of mission-critical products a wider berth when negotiating prices.

IBP has about a dozen sell-side analysts covering it, which is good coverage for a mid-cap name. One likely reason for the interest is that the sell-side’s associated investment banks are attracted to the acquisitive nature of IBP’s business. I still consider it an overlooked name, primarily because it’s a $5 billion B2B operation with a decentralized business model that isn’t well known to most consumers and investors.

Or perhaps it’s just because I hadn’t heard of it before.

In any case, let’s dig into the details around IBP’s moat and management, my scores for these qualitative categories, and address what a reasonable valuation might be for the company.