Flyover Stock: Donaldson (DCI)

This Minnesota-based filter specialist stands to benefit from increased emissions pressure on heavy transportation equipment.

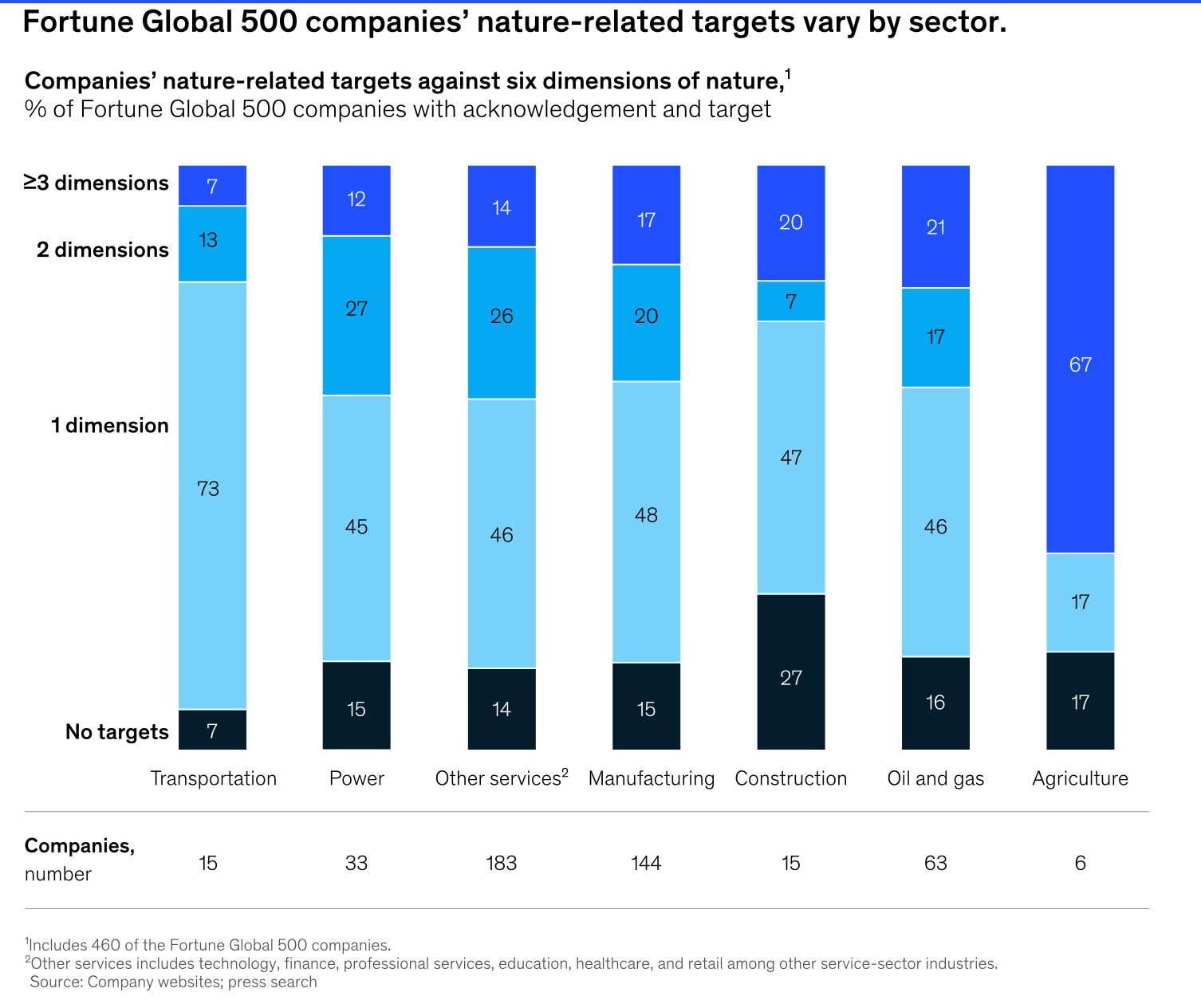

With over 80% of Fortune 500 companies committing to sustainability and emission-reduction targets, it stands to reason that suppliers that help them achieve those targets stand to benefit.

This is particularly true for industrial companies that produce or use fossil-fuel-intensive machinery.

Indeed, the U.S. Environmental Protection Agency (EPA) is applying more stringent standards for heavy machinery emissions starting in 2027, which also requires OEMs to extend engine life. The regulations become more stringent in following years.

It's also apparent that gas-powered heavy machinery and transportation will play an essential role in the coming decades. The weight of electric batteries necessary to power tractor-trailers, for example, is so considerable that road and bridge weight limits reduce the trucks' haul capacity.

While there are some battery-powered prototypes in heavy (non-passenger) vehicles for construction, mining, and agriculture, they will likely slowly take share due to replacement cycles, proof of concept, and weight concerns. In agriculture, for example, heavier tractors can damage soil, and downtime required for battery charging during harvest season is a huge opportunity cost for farmers.

“Today the reason why most agricultural machinery is [run by] diesel is because of the high power-to-weight ratios when we look at energy storage in the form of diesel fuel…(Large equipment) can work all day without having to refill.”

- Scott Shearer, chair of the Department of Food, Agricultural and Biological Engineering at Ohio State University

Today's profiled company, Donaldson, is helping its OEM customers meet regulatory and sustainability targets from ICE- and diesel-powered machinery. It is also positioning itself to benefit from emerging alternative fuels and life sciences technologies.

For 109 years, Donaldson has produced high-technology filters that remove dust and other contaminants to better protect and extend the life of expensive machinery.

Despite selling into cyclical end markets, Donaldson's business has proven resilient. It's increased its dividend for 28 consecutive years, encompassing the financial crisis and COVID years – two periods that saw many dividend streaks end.

Its resiliency can largely be attributed to its razor-and-blade business model, in which Donaldson filters are included in an OEM design and then regularly replaced over the equipment's life.

Let's take a closer look at this Minnesota-based company's moat, management, and valuation, along with Flyover Stock rankings across six categories.