ESG Investing: Be Curious, Not Judgmental

Call it ESG, sustainability, or transition investing - the underlying principles are important for thoughtful investors to consider

I recently obtained the CFA Certificate in ESG Investing. I pursued the certificate because, as the faculty advisor to a student-managed ESG fund, I wanted to better understand the topics germane to the approach.

It had the pleasant side effect of providing new angles for considering long-term and terminal risks to the businesses I research.

Now, I know those three letters can be eye-roll-inducing to some, and I can appreciate that. The ESG bubble of recent years has, at times, crossed the lines into politics and culture wars and made it a divisive topic.

This recent video from the FT is an excellent summary of what’s happened in the ESG industry.

Indeed, investors have soured on ESG-themed investing and flows to such funds have dried up.

It’s not the purpose of this post to get into the reasons for that shift, but whether you want to call it ESG, sustainability, transition, or something else, the underlying concepts are here to stay and are therefore worth considering.

The bubble in ESG investing, to borrow a phrase from Seth Klarman, was a good idea carried to excess. The excess may have dissipated but the good ideas remain.

I can also tell you from first-hand experience that the upcoming generation of investment professionals cares deeply about environmental and social matters. If you’re keen to attract and retain this group, it’s worth knowing and applying ESG concepts.

Regardless of your opinion on climate change, it makes good business sense for companies to promote sustainable activities that benefit as many stakeholders as possible.

When I watched the video below on James Dyson’s sustainable farming practices in the UK, for example, it struck me how energy sustainability can mitigate risk (less dependence on global energy markets), increase resilience, and potentially provide a competitive advantage in the event of a disruption in global energy supply.

What’s more, as long-term investors forecasting cash flows years and decades ahead, we need to consider our companies' (implied or explicit) terminal values.

In a discounted cash flow model, terminal value assumptions often account for more than half of our fair value estimates. Slight changes in these assumptions can, therefore, have meaningful impacts on our valuations. If we misjudge long-term growth and risk inputs, our estimates will be well off course, and our capital will be at risk of impairment.

As such, we should care about how our companies are managing waste and emissions, caring for employees and their communities, and practicing good corporate governance. These are all relevant long-term concerns that can impact - good or bad - a company’s economic moat.

Milton Friedman famously argued that companies have only one responsibility—to increase profits. We can debate whether companies have the responsibility to be good environmental and social stewards, but they should really want to be those things in first place. It doesn't have anything to do with ESG as a theme—it's just good business.

Whether its “dancing” while the subprime music played or improperly disposing dangerous chemicals, investors should aim to avoid companies trying to do unsustainable things sustainably. This creates off-balance sheet liabilities that can come due at any moment.

Companies that are not good environmental and social stewards are unlikely to be good stewards of our capital over the coming decades. Taking shortcuts (underpaying labor, not investing in renewable energy sources, etc.) might boost margins and ROIC today, but could make the company less competitive in the coming decades.

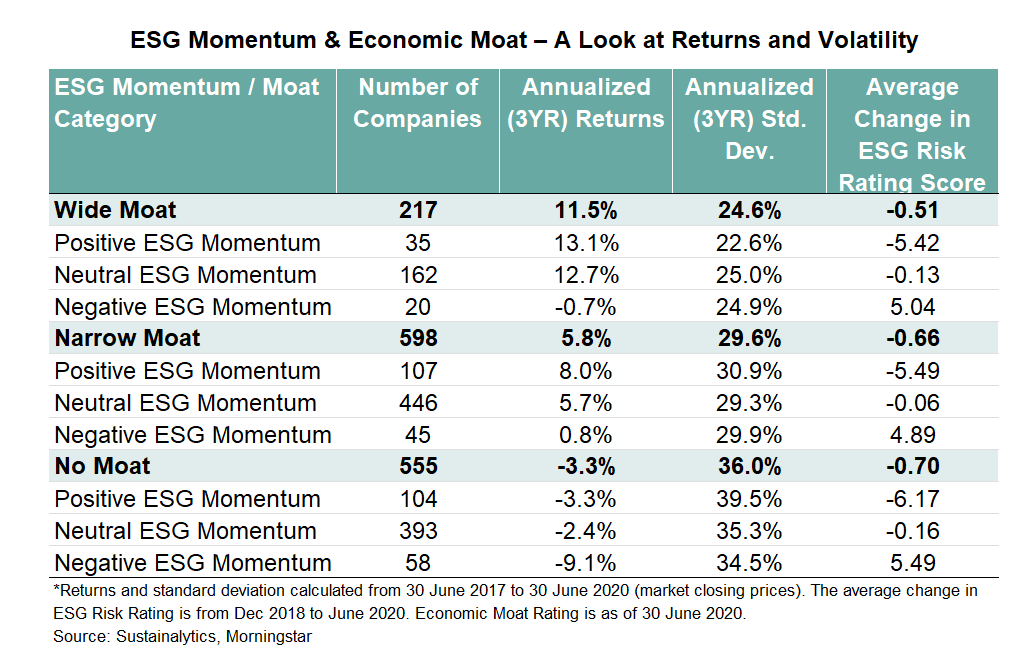

In 2020, Morningstar and its subsidiary, Sustainalytics, released a study that showed that companies with negative ESG momentum (score declined by at least three points) posted relatively poor annual returns as a group. Conceptually, this makes sense. While companies should be analyzed individually, those with declining ESG scores should be get additional scrutiny to see if anything is amiss.

To be sure, considering the materiality of a company’s sustainability practices is not easy. Some companies are more forthcoming and transparent than others, there is often a low positive correlation between third-party ESG scores, and greenwashing is a perennial problem.

A good starting point for research is considering a company’s relationship with and the value it provides to its various stakeholders. Put yourself in the shoes of employees, customers, suppliers, and communities connected to the company and ask questions like:

Would you want to be a supplier to this company?

Would you encourage a loved one to apply for a job there?

Was the company reinvesting in its communities and acting as a good environmental steward before the ESG money started flowing a few years ago?

Another angle to consider is how a company’s sustainability efforts align with its existing competitive advantages or moat sources.

For example, Costco has long been generous with its pay and benefits for warehouse employees. While there may be some altruism to that policy, it also supports the company’s moat. Happy employees better serve members, satisfied members are more likely to renew their membership and encourage others to do the same, satisfied members shop more and support the company, which enables the company to hire quality employees and keep them happy. The cycle repeats.

"When employees are happy, they are your very best ambassadors."

- Costco founder, Jim Sinegal

Every company has its blemishes and points for criticism, but what you should try to determine is if the company acknowledges those weak points, how material they are to the business’s risks and opportunities, and what it’s doing to address them.

If a company is defensive about its governance practices (e.g., board is too small, independence is questionable, etc.), for example, then that’s a sign to either engage with the company in an effort to improve their governance or exit the position.

In the coming decade, companies will also pay more attention to the environmental impacts of their upstream and downstream value chain, often referred to as Scope 3 emissions. To illustrate, if your company isn’t emitting much GHG (Scope 1) and is only using renewable energy (Scope 2), but one of your biggest customers uses your product to generate large amounts of GHGs, then your Scope 1 and 2 emissions will be low, but you Scope 3 emissions will be high.

Accounting and Reporting Standard")

It’s debatable as to whether a company should be responsible for the GHG emissions of its suppliers or customers, but it’s nevertheless a risk worth noting. If one of your biggest customers is adding an off-balance sheet liability, it could come back to hurt your business.

Consequently, I expect to see more companies - especially larger, multinational companies - apply more pressure on their value chain partners to reduce emissions and become more sustainable in general. Companies that help their suppliers and customers achieve this goal likely have a tailwind in the years ahead.

I expect skepticism and controversy around “ESG” to continue, but as with most politicized topics, it’s a sideshow to a more important matter. Those who have pushed for ESG principles in investing have done the industry a service by helping professionals develop a framework for considering key risks and opportunities.

Ultimately, what we call ESG analysis today will blend into just “analysis.” For now, it remains a distinct approach in the industry. You may not feel the need to do an ESG investing exam like I did, but I encourage you to be curious about the principles behind ESG and how you might apply them to your process.

Stay patient, stay focused.

Todd

Todd Wenning is the President and CIO at KNA Capital Management, LLC, an Ohio-registered investment advisor.

Todd can be reached through this contact form.

At the time of publication, Todd, his family, and/or KNA Capital Management owned shares of Costco.

All information contained herein is provided “as is” and KNA Capital Management, LLC (“KNA”) expressly disclaims making any express or implied warranties with respect to the fitness of the information contained herein for any particular usage, application or purpose. Prior to making any investment decision you should consult with professional financial, legal and tax advisors to determine the appropriateness of the risks associated with such an investment. No assurance can be given that the objectives of a particular investment will be achieved or that an investor will receive a return of all or part of his or her investment. All investments involve the risk of loss, including the loss of principal. In no event shall KNA be responsible or liable for the correctness of any material used herein or for any damage or lost opportunities resulting from the use of such material.

Users of this content may not reproduce, modify, copy, alter in any way, distribute, sell, resell, transmit, transfer, license, assign or publish any information obtained through this website without permission. KNA and the terms, logos, and marks included herein that identify KNA products are proprietary materials. The use of such terms, logos, and marks without the express written consent of KNA is strictly prohibited.

Disclaimer:

Todd is the President and CIO of KNA Capital Management, LLC, an investment management firm based in Cincinnati, Ohio that is currently pending state registration. The information contained on this site as well as kna-capital.com is for informational purposes only and should not be considered as investment advice or as a recommendation of any particular strategy or investment product. This blog should not be considered as a solicitation for services.

This material on FlyoverStocks.com is published by W8 Group, LLC and is for informational, entertainment, and educational purposes only and is not financial advice or a solicitation to deal in any of the securities mentioned. All investments carry risks, including the risk of losing all your investment. Investors should carefully consider the risks involved before making any investment decision. Be sure to do your own due diligence before making an investment of any kind.

At time of publication, the author, his family, or KNA Capital Management clients may have an interest in the securities mentioned or discussed. Any ownership of this kind will be disclosed at the time of publication, but may not be updated if ownership of a particular security changes after publication.

This newsletter does not provide buy or sell recommendations and articles should not be interpreted this way.

Information presented may be sourced from third parties and public filings. Unless otherwise specified, any links to these sources are included for convenience only and are not endorsements, sponsorships, or recommendations of any opinions expressed or services offered by those third parties.

Flyover Stocks has partnered with Koyfin to provide a discount to Koyfin’s services for Flyover Stocks readers. The W8 Group, LLC, which publishes Flyover Stocks, may receive a commission from a reader’s purchase of products linked from this page as part of an affiliate program.