Dividend Investing is Dead

Three structural shifts that broke a centuries-old playbook, and how to adapt your portfolio.

10 years ago, I wrote a book on dividend investing. Six years prior to the book, I ran a dividend-focused investing newsletter in the UK.

Suffice it to say, I’ve thought a lot about dividends over the years.

Early in my career, I was greatly influenced by research on dividends, including Robert Arnott and Cliff Asness’s paper on how higher dividend payout ratios led to faster earnings growth, and Jeremy Siegel’s book The Future for Investors, which showed that many of the best performing stocks from the previous half century were generous dividend payers.

Dividend investing meshed well with my conservative nature and with the quality-value approach that I was developing.

Here are some of my key takeaways from my research:

Companies need cash flows to pay dividends, not GAAP accounting opinions.

To increase the dividend, boards need to be confident in the company’s ability to generate more cash flows.

Growing dividends are suggestive of a competitive advantage, since the board must be confident in the company’s ability to generate higher future cash flows.

Growing dividends indicate the board’s interest in sharing the company’s prosperity with shareholders.

Dividends reduce the size of the management’s sandbox, forcing them to be more focused with capital allocation decisions.

The goal of dividend investing, I concluded, was to build a well-diversified portfolio of well-covered dividend-paying stocks with a targeted yield of 3-4% and free cash flow per share growth of 6-7%. Over time, this would produce market-like returns with less volatility.

10 years ago, this seemed achievable, though I sensed a change on the horizon, which is why I titled the book Keeping Your Dividend Edge.

In the book’s conclusion, I wrote:

The days of “buying and forgetting” dividend-paying stocks are over – if they ever really existed. In today’s market, new and existing competitors alike are looking to disrupt high-margin, cash-flow generating businesses that are resting on their laurels. If a company’s advantages are slipping, its profits and cash flows come under pressure and the dividend could therefore be at risk. Due to the ever-increasing competitiveness of the global markets, we can’t remain ignorant of a company’s competitive position and expect to do consistently well.

In theory, all of these lessons I took from dividend investing remain valid today. But holding onto the “edge” that dividend strategies offer has become less secure. The environment changed in three important ways that make dividend investing as described above impractical going forward.

Disrupted consumer staples

For one, many of the consumer staples giants that served as anchors in high-dividend yield portfolios have been challenged in an age of advertising disintermediation and GLP-1s altering consumer behaviors.

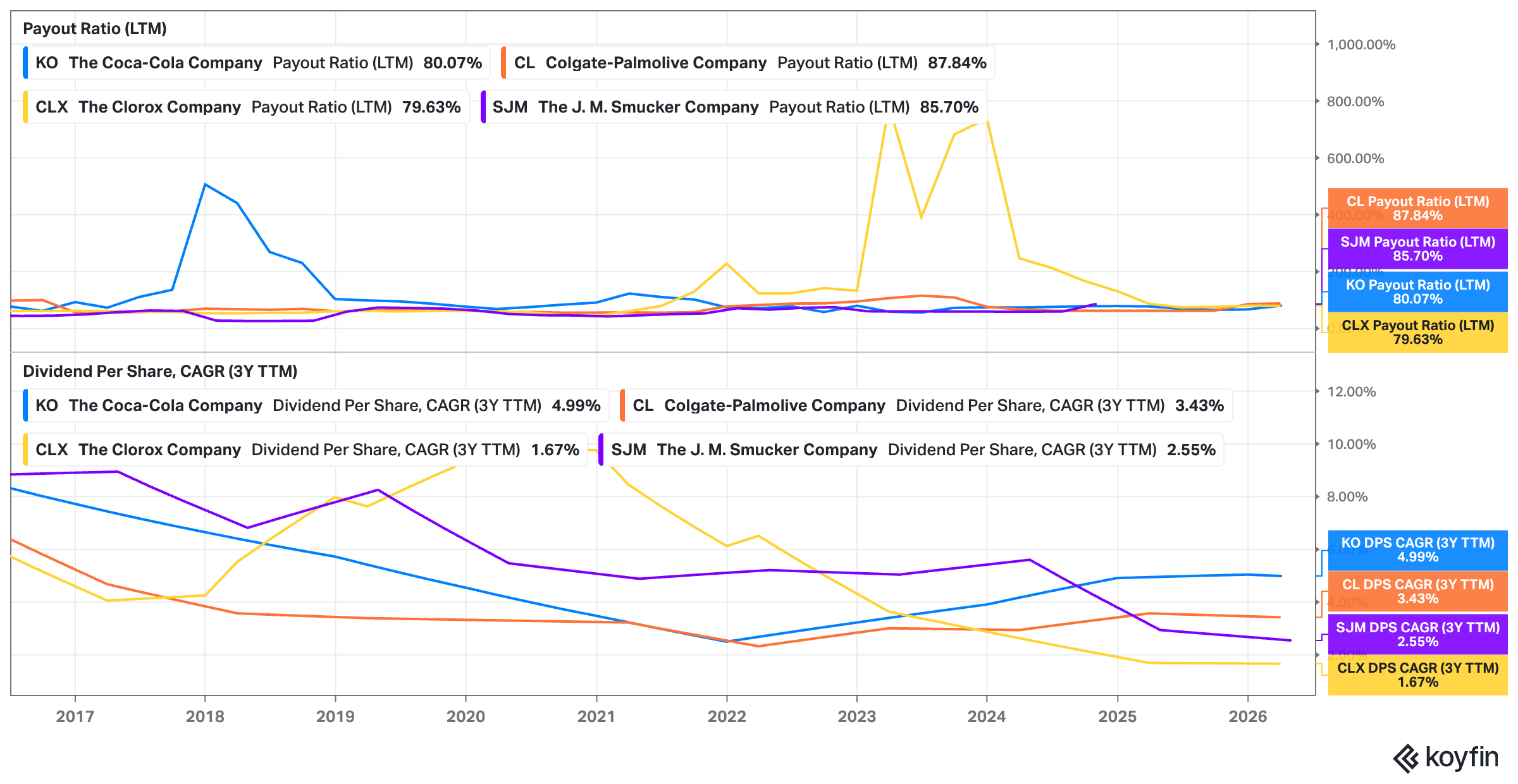

These dynamics have shown up in consumer staples dividend growth rates.

Consider the declining three-year trailing dividend growth trends for Coca-Cola, Colgate-Palmolive, J.M. Smucker, and Clorox - four “Dividend Aristocrats” that have grown their dividends each year for 25+ years.

For years, dividend investors could rely on big consumer brands to be defensive and consistent, but the rise of influencer marketing and private label (e.g. Costco’s Kirkland) and GLP-1s have changed the game. What’s more, these disruptive factors have forced a change in capital allocation priorities. But with each of the above stocks - and many more in the sector - paying out 75% or more of their earnings in dividends each year, the CFOs are handcuffed when making allocation decisions.

A slashed dividend by an Aristocrat would not only confirm there’s trouble but would also mean the stock is dropped from many high-AUM dividend-focused investment pools. As such, boards are reluctant to make the call, even if it’s the optimal long-term strategy.

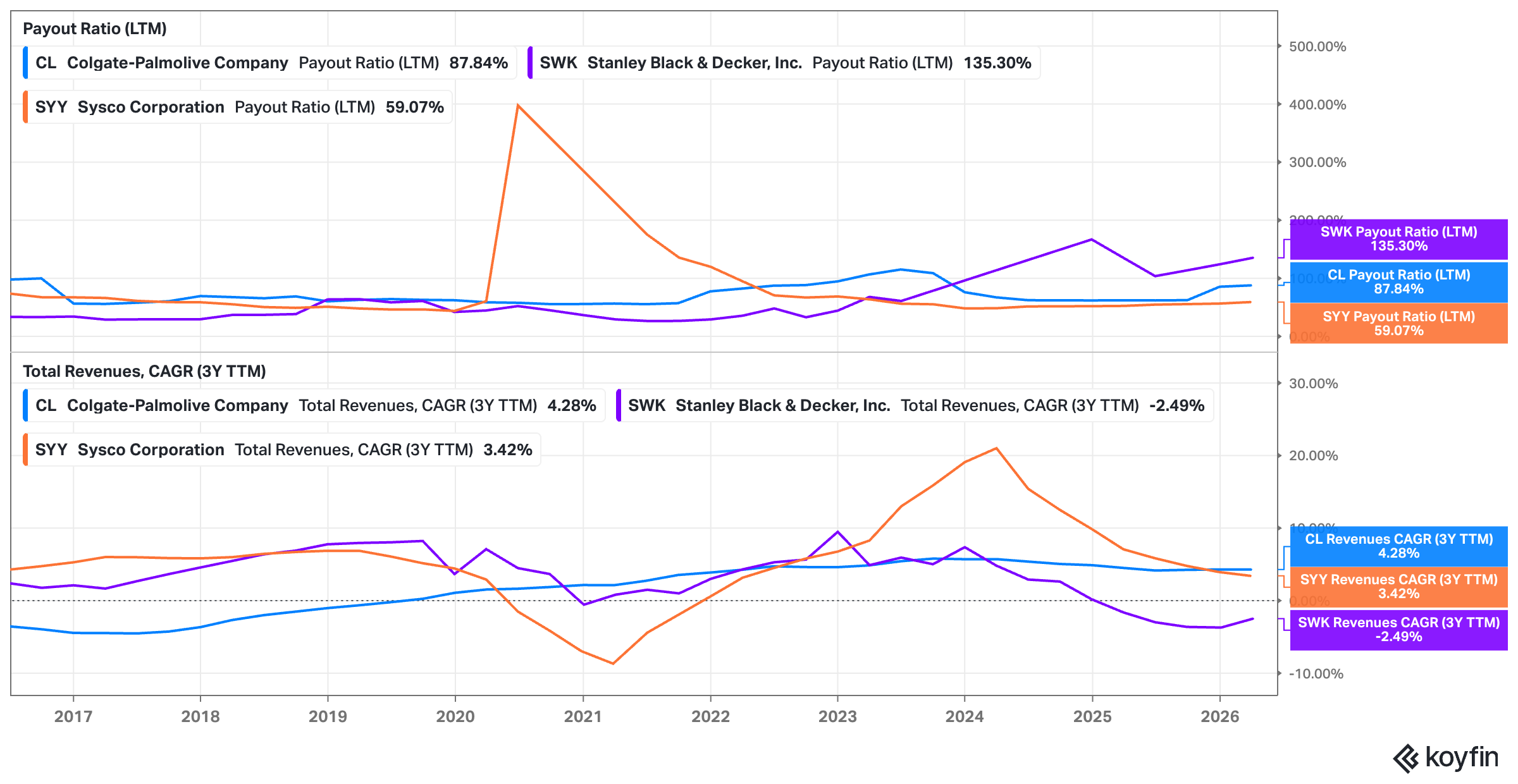

(As an aside, I roll my eyes when I see Aristocrats raising their dividends by one measly cent to avoid being kicked off. Colgate-Palmolive, Sysco, and Stanley Black & Decker have all done it in just the past year. I can't think of a better sign that a board is worried about the dividend, hoping the company catches a break to rebuild its stretched coverage ratios before the next review.)

Liquor companies, which were supposed to be the ultimate defensive consumer staples category, have run into hard times post-COVID. Even five years ago it would have been unthinkable that Diageo - owner of the Johnnie Walker, Guinness, and Tanqueray brands - would cut its dividend anytime soon, and yet that’s exactly what happened earlier this year.

Changing board dynamics

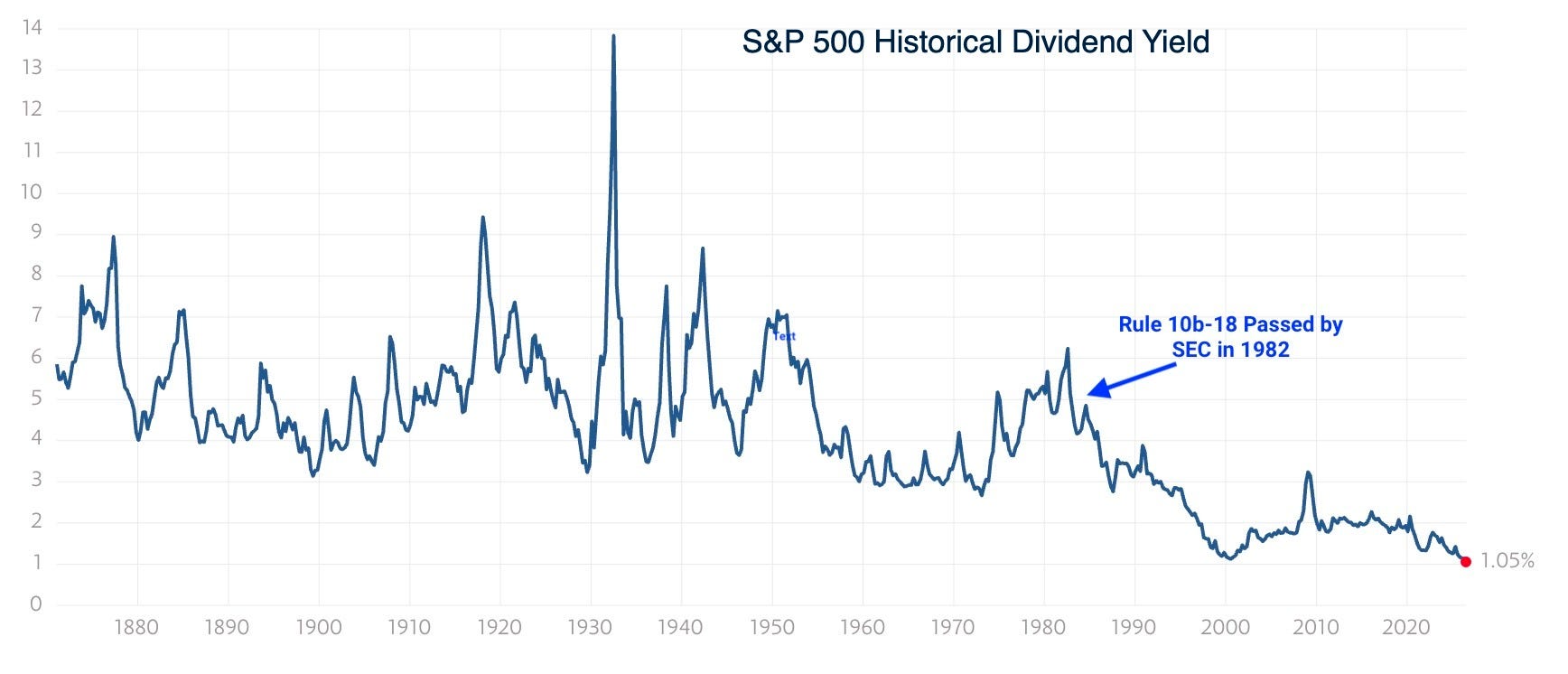

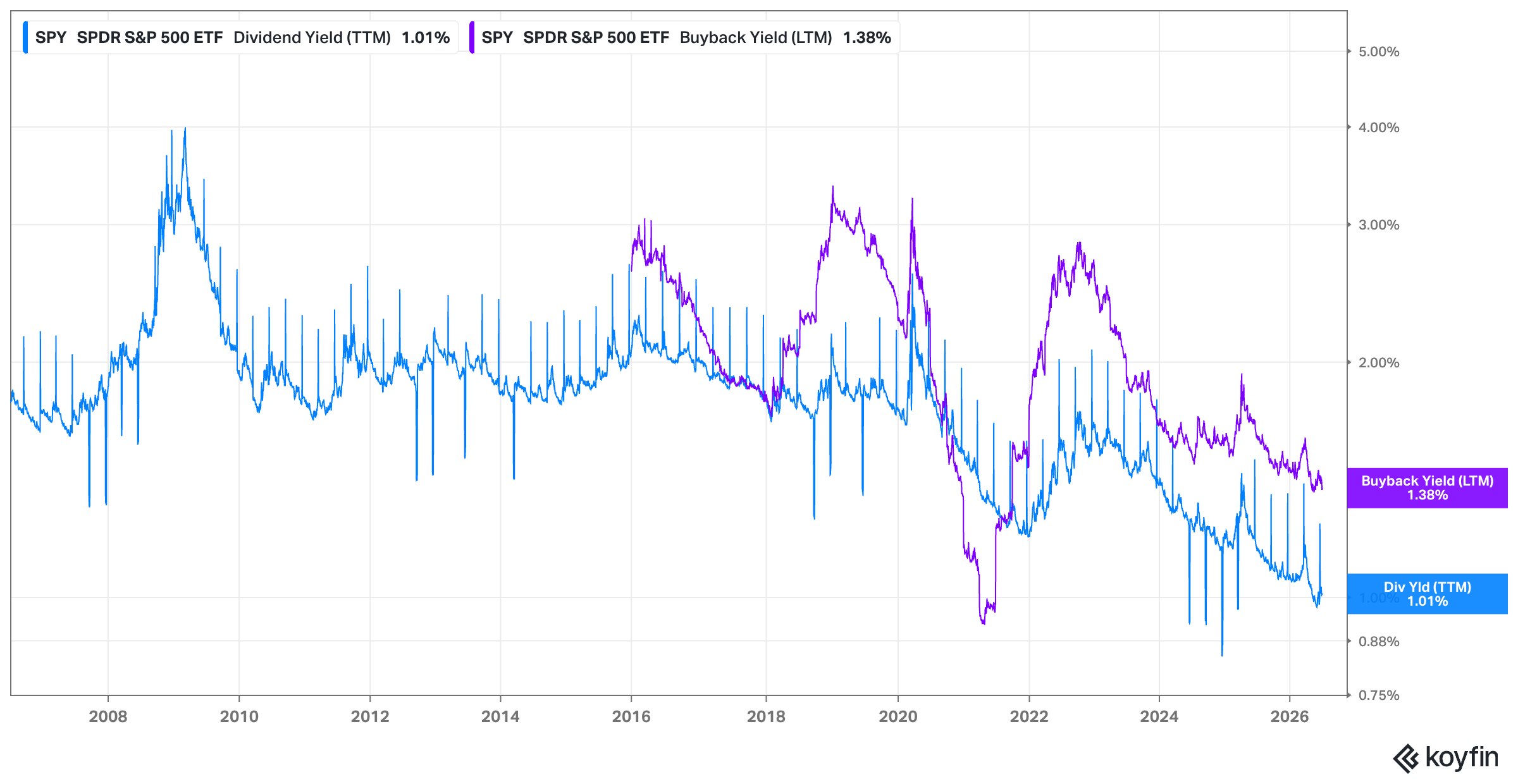

Since 1982 when SEC Rule 10b-18 passed (allowing companies more freedom to make share repurchases), there’s been a material shift in how companies prefer to return cash to shareholders.

Indeed, for most of the past decade, the S&P 500’s buyback yield had exceeded that of the dividend yield.

Compared with dividends, which in the US comes with an implicit commitment to pay at least as much in subsequent years, buybacks offer more flexibility. In tough times, the company can retain cash. If the stock is cheap, the company can buy stock and increase the ownership slice of ongoing shareholders.

Indeed, in the hands of a skilled allocator, buybacks are preferable to dividends. The opposite is also true, of course. Poor allocators can destroy value with buybacks if they are overpaying for shares.

In taxable accounts, buybacks are more tax efficient than dividends. Dividends are taxed when paid while capital gains are deferred until a sale. Naturally, this demands prudent asset location from investors and advisors to hold low- or no-yielding compounders in taxable accounts while sheltering higher-yielding stocks inside qualified accounts.

As board members of public companies cycle in and out, the memory of pre-1982 capital allocation priorities fades. To illustrate, the average age of new board members is 59. This group would have been 15 years old when SEC Rule 10-b 18 passed.

Consequently, as time passes, boards become more comfortable with buyback-first capital allocation policies. The case for dividends becomes an uphill battle, especially at firms without a long dividend paying history.

Even the 1% buyback tax introduced by the 2022 Inflation Reduction Act may have had a small initial impact on buyback activity as companies weighed the costs, but buyback activity has resumed its pre-IRA trendline.

In short, the buyback train keeps rolling. Save some massive government policy change, it’s hard to imagine it slowing down anytime soon.

The rise of technology

Since the 1950s, the average age of an S&P 500 constituent has declined from 57 years to 15 years. This trend is due to a number of factors, including disruption, failure, acquisition, and younger, rapidly growing (mainly) technology companies kicking out slower more mature businesses in the index.

Over the last decade, for example, exits from the S&P 500 include Campbell’s (founded 1869), Newell Brands (1903), Macy’s (1858), Xerox (1906), and Harley-Davidson (1903), all of which at one point in their histories had generous dividend policies.

Younger companies that replace these names tend to be in their high-growth phase where dividends are naturally less attractive. Further, the companies did not exist in an era where shareholders preferred dividends. There is little incentive for them to start paying one now.

AI only throws kerosene on this trend. Powered by AI, companies can be started faster than ever, challenging today’s mature companies to defer dividends into reinvestment to keep upstarts at bay. Similarly, established competitors looking to take back share can use AI tools in new and creative ways to disrupt the status quo.

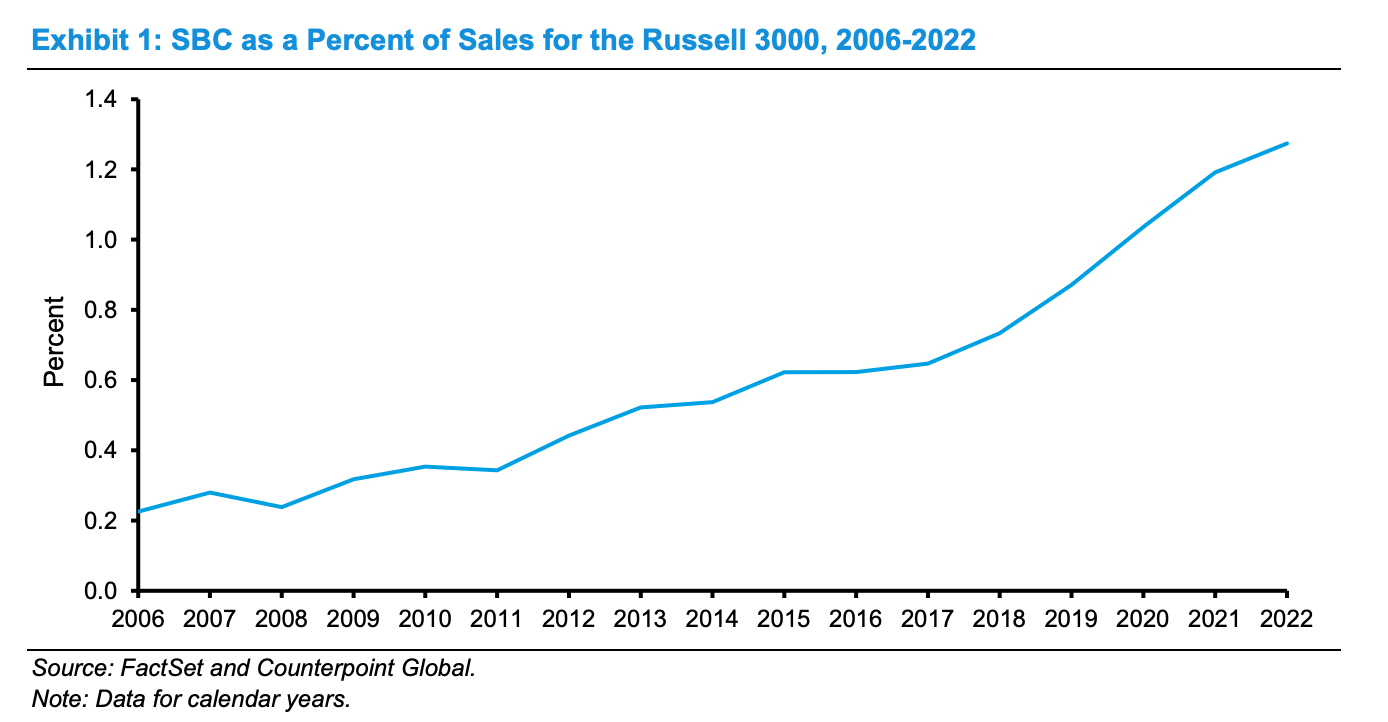

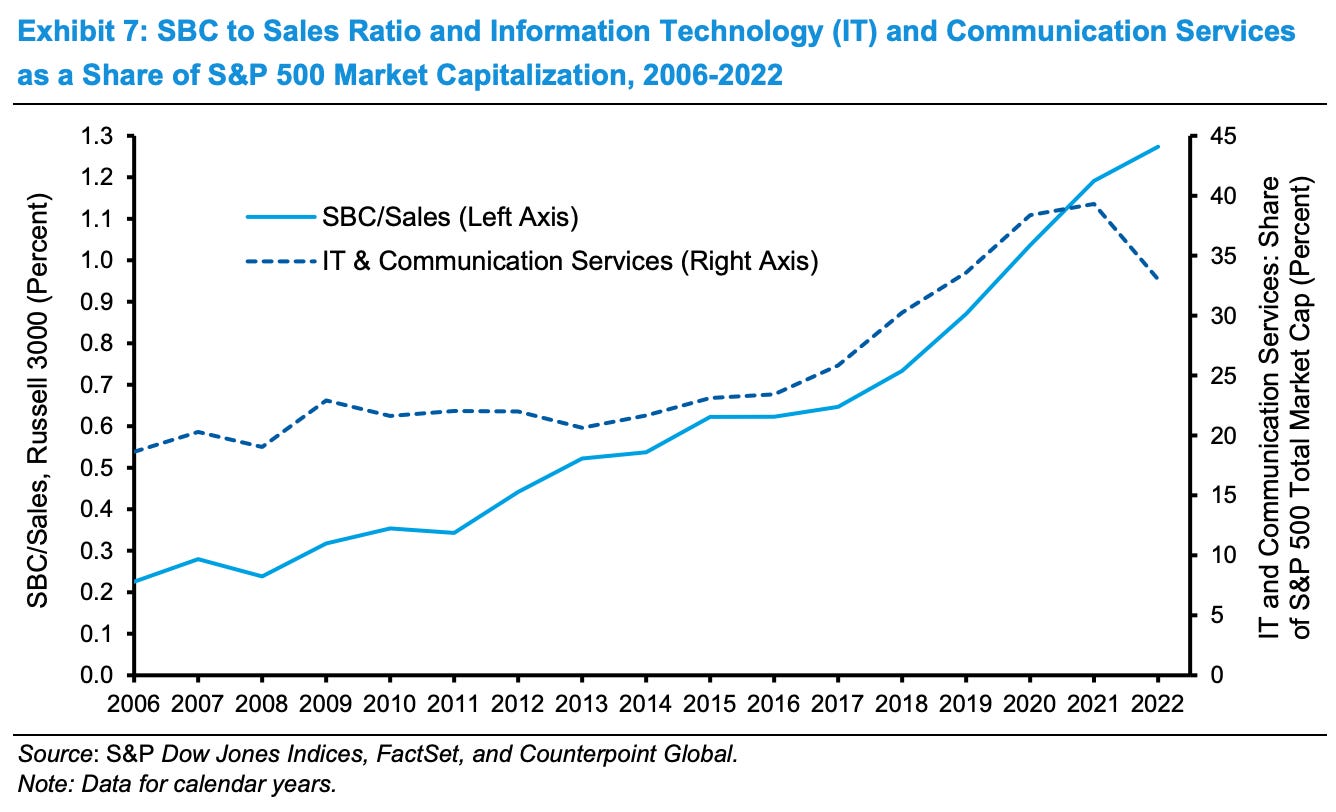

Younger companies also increasingly use buybacks to offset the increased use of stock-based compensation, which has become increasingly prominent among the growing technology sector, as illustrated in this paper by Michael Mauboussin and Dan Callahan.

As long as companies see SBC as a key part of employee compensation, they’ll need to divert free cash flow toward offsetting SBC’s dilutive properties. This reduces the amount of free cash available as dividends to shareholders.

Putting it together

The dividend investing world that existed 20 years ago is long gone and I don’t think it’s coming back.

To be sure, distributing cash a business can't productively reinvest hasn't died at all, but the preferred mechanism for returning cash has shifted away from dividends and toward buybacks.

This isn’t to say that dividend investing strategies won’t find success, but they will require investors and managers to select from an ever-smaller set of companies committed to returning generous amounts of free cash flow each year in the form of cash payouts.

Consequently, investors drawn to dividend investing will need to adjust, if they haven’t already.

Focus on the way management allocates all of its cash flow.

Track record: Does management have a history of using cash opportunistically or pro-cyclically?

Reducing or diluting: If the company buys back a lot of stock each year, is it actually reducing the share count or just diminishing the impact of SBC dilution?

M&A discipline: Have acquisitions been prudent or does management have a history of taking regular restructuring or impairment charges?

Focus less on the company’s history and more on its ability to adjust to change.

Balance sheet strength: Does the company have a strong balance sheet to respond to new opportunities and stay focused on long term strategies in times of change?

Moat stability: How wide is the company’s moat and does it give management time to respond to new threats?

Corporate culture: Is the company’s culture flexible and adaptive or are the hallways filled with people doing the bare minimum?

Be mindful of mental accounting

If you own a company that’s buying back a percentage of its shares each year, why not sell off that percentage of your holdings to generate income?

Nothing in markets stays the same forever. For over a century, dividends were the primary means for companies to return shareholder cash and many mature businesses’ capital return policies were developed during that time.

That’s no longer the case. Any company that’s gone public since 1982 in the US has had free use of buybacks as an alternative. Global competition has never been more intense and boards are reluctant to implicitly commit a large percentage of earnings when they may need the capital to respond to changes.

It’s true that dividend yields would naturally become more attractive if the market sharply sells off; however, that doesn’t mean dividend investing would be back.

Given what we discussed so far, such a downturn would provide boards that are already anxious about their current dividend policy the cover they need to cut their current payouts. We saw some of this behavior during the financial crisis - Dow Chemical, Pfizer, General Electric, to name a few. Their distinguished dividend-paying heritages didn’t mean anything. If dividend cuts become acceptable in a certain window, companies with stretched policies can seize the opportunity to reevaluate.

Bottom line

I’ll reiterate that all the positive attributes of dividend investing I mentioned in the bullet points above are still true. In theory.

But dividend investing, as I knew it and loved it, is dead.

Destroying your best-loved ideas, using Charlie Munger’s phrasing, is not an easy thing to do. The ideas were best-loved for a reason. But times change, and so must we.

Stay patient, stay focused.

Todd

Enjoyed this article? I write for investors who care more about process than predictions and regularly share thoughts on individual companies on my radar.

Join over 12,700 thoughtful investors who read Flyover Stocks.

Todd Wenning is the President & CIO of KNA Capital Management, LLC, an Ohio-registered investment advisor that manages a concentrated equity strategy and provides other investment-related services.

At the time of publication, the author, his immediate family, and/or KNA Capital Management, LLC or its clients do not have positions in any company mentioned.

Please see important disclaimers.