Two Beaten-Up SMID Caps on My Radar

With the market's attention remaining on large cap growth, looking for opportunities among overlooked SMID caps is a good place to start.

If you enjoy this post, please like or share it to encourage more thoughtful investors to join the Flyover Stocks community!

While the S&P 500 and Nasdaq 100 are positive year-to-date, SMID Cap (small- and mid-cap) stocks as a group have languished.

As the chart below illustrates, the major mid-cap and small-cap indices (thicker lines) have underperformed the S&P 500 (SPY), with only the S&P 500 Growth (IVW) fortified with AI beneficiaries outperforming the standard bearer.

While the market’s attention is on large cap growth names, it’s worth looking through the beaten-up SMID cap space in search of quality names worthy of further research.

To augment and accelerate my research, I’ll implement an AI-driven research platform called Tenzing MEMO. In 2022, my friend Nick Kapur launched the platform with Tom Saberhagen, a former partner and co-portfolio manager at Akre Capital, as a way to keep tabs on a large universe of companies with the limited resources of a small firm.

Tenzing MEMO recently launched version 2.0, which features an improved mobile interface, chat history, and an additional 1,000+ research-ready stocks. I find the valuation and governance sections particularly useful when I’m looking at a company for the first time.

Professional investors who are interested in a free trial to Tenzing MEMO can register on the Tenzing MEMO website (all new users receive a generous, no commitment free trial to kick the tires of the software). Tip: register with your work email for expedited service.

As an added bonus, Tenzing is generously offering Flyover Stocks members an additional 10% off yearly subscriptions. Based on the pricing of various platforms I’ve been pitched over the years, their rates are quite reasonable given the breadth and depth of the available data.

You can sign up for a free trial here, and if you like it enough to buy it, reference code FLYWITHUS to receive the extra 10% off your annual subscription.

Additional disclosure: I have an established partnership with Tenzing MEMO for which I may receive a commission on product sales. I only promote third-party products that I use and enjoy. Please see important disclaimers.

Landstar System (LSTR)

Market cap: $4.81 billion

P/E (ttm): 27.3x

Dividend yield: 2.5%

Headquarters: Jacksonville, FL

Landstar is a freight broker that matches shippers and freight operators through an extensive independent agent network. It primarily operates in the van and unsided (i.e. flatbed) truckload (TL) freight market, though it is able to match freight via ocean, air, and rail as needed.

Two attractive aspects of Landstar’s business model are:

Business Capacity Owners (BCOs): While Landstar sends a lot of business to third-party drivers, Landstar has a “captive” group of independent drivers called Business Capacity Owners that haul exclusively for Landstar. Every BCO has Hazmat certification and can haul most types of freight. The BCO model is mutually beneficial to Landstar and the independent owner-operators. BCOs get first dibs on jobs, so they have assured business across the freight cycle. Consistent work is critical to independent truck drivers, which have high fixed costs. Landstar benefits from higher margins on jobs pushed to BCOs and having a trusted network of drivers.

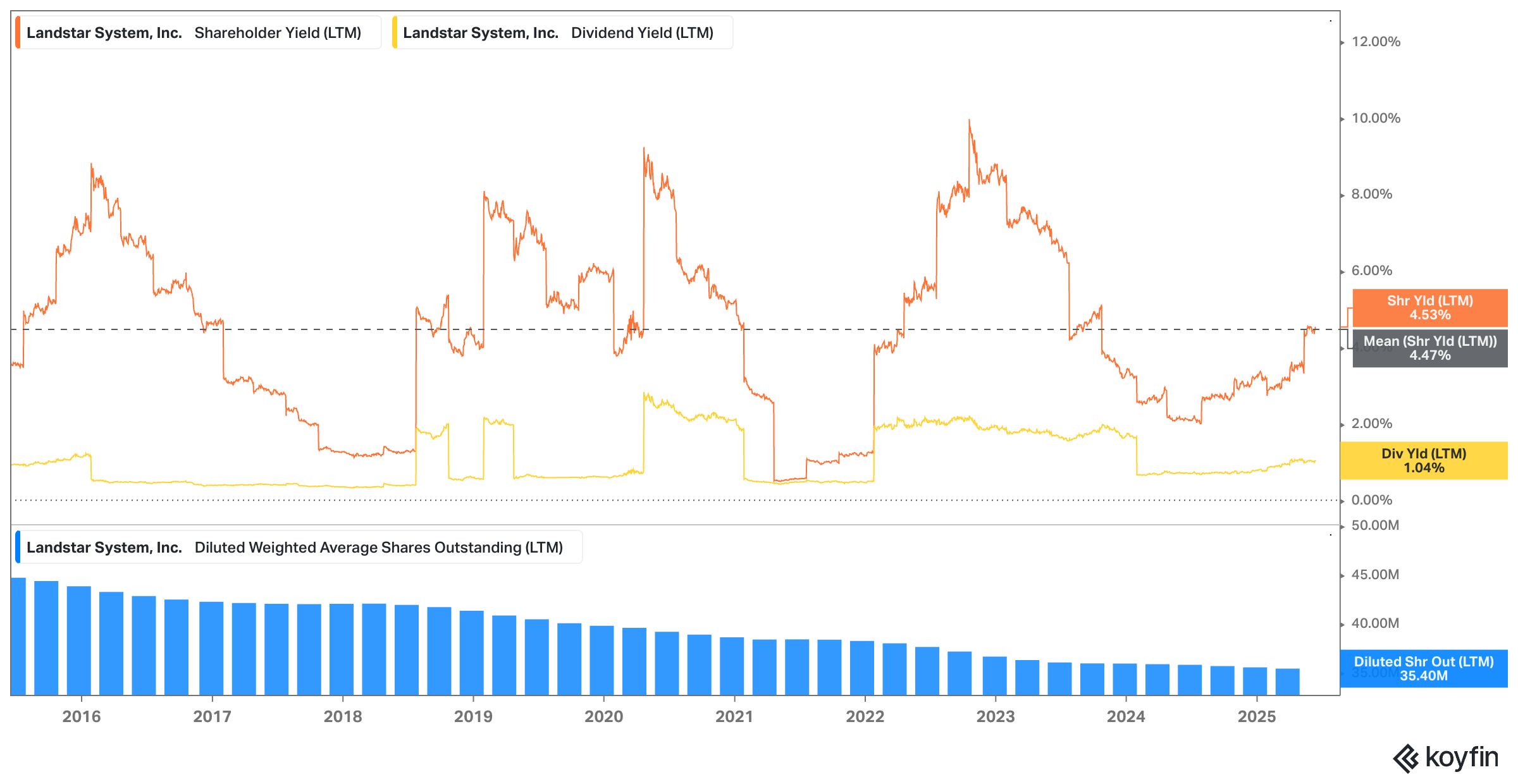

Asset-light: Unlike many of its competitors in the TL logistics space, Landstar doesn’t own any tractors. It owns some trailers that it leases primarily to its BCOs. Because capital expenditure needs are minimal, Landstar generates considerable free cash flow, which it has historically used to buyback stock, pay a small regular dividend, and occasional special dividends.

Despite these positive attributes, Landstar’s stock has struggled over the past year due to concerns about international trade and tariffs, declining U.S. freight rates, and more recently, a significant incident of supply chain fraud by one of its international agents.

I asked Tenzing MEMO for more details on the case:

In late Q1 2025, Landstar discovered a significant supply chain fraud within its international freight forwarding operations—distinct from its core North American truckload business. The fraud was isolated to a single independent agent office and involved misappropriation related to trade accounts receivable. Landstar took a $4.8 million pre-tax charge ($0.10 per share) in Q1 2025 to reflect the anticipated financial impact, net of some expected recoveries. The company delayed its Q1 10-Q filing to address related accounting and internal control issues, prompting several law firms to launch securities fraud investigations. Management emphasized that the fraud was not systemic, was limited in scope, and that remediation and collection efforts are ongoing. No further significant charges are expected, aside from legal and professional fees. The incident raised concerns about internal controls but did not affect Landstar’s core operations or financial stability.

Having followed Landstar on and off again for eight years, I would lean toward the supply chain fraud indeed being an isolated incident, but risks related to independent agents remain.

The other factors affecting Landstar’s stock today are mainly cyclical in nature. Landstar’s trailing P/E of 27.9x is deceptive due to these cyclical factors, which have depressed the earnings per share. If we take the average 10-year ROE of 32.9% and multiply it by the current book value of $26.63, it suggests normalized EPS of $8.76, or 15.7x based on the stock price at the close on June 13. Landstar’s average P/E over the last decade is 22x, making this an interesting time to dig into the name.

Two negative secular trends worth monitoring, however, are surging insurance expenses (Landstar covers the insurance on BCO hauls), which cut into margins, and the persistent threat of digital-only freight brokerages like Uber Freight. Landstar management has long argued that they have the same technology on their own mobile app and that digital-only is best used for transporting low-cost goods. When transporting expensive goods like industrial equipment or hazmat, shippers still want someone to talk to while the items are in transit.

One of the new Tenzing MEMO features that I’ve enjoyed recently is called “The Skeptic” which essentially plays the “red-team” role, aiming to challenge bullish points and find weaknesses in the business. It has a curmudgeon personality, but often brings up important considerations.

For Landstar, “The Skeptic” calls out Landstar’s capital allocation in recent years, which has featured ongoing buybacks and special dividends in the midst of rapid technological innovation in freight brokerage. The lack of reinvestment could render Landstar’s platform obsolete, it argues.

It’s an important point, but as noted above, Landstar’s asset light business model means it generates a lot of free cash flow and has little reinvestment needs. To management’s credit, it has reinvested in technology, which it feels is comparable to other platforms.

Ingles Markets (IMKTA)

Market cap: $1.1 billion

P/E (ttm): 18.6x

Dividend yield: 1.1%

Headquarters: Ashville, NC

The devastation wrought by Hurricane Helene in September 2024 can still be seen across the Ashville, North Carolina area. Interstates and major roads are still being repaired, slowing traffic through the region. Debris and downed trees are still piled up in places. Damaged stores have yet to be reopened.

This includes three Ingles grocery store locations, which are expected to reopen later this year.

The 198 Ingles Markets locations can be found across the Southeastern U.S., including 75 in North Carolina, 65 in Georgia, 35 in South Carolina, and 21 in Tennessee. Despite the regional diversity, Ingles was impacted particularly hard by Helene due to its headquarters being in Ashville, which is also the center of its store and distribution network.

At face value, Ingles is a typical regional grocery store, facing similar competitive pressures from the likes of Wal-Mart and Costco, but it has a number of differentiating attributes compared to other regional grocers.

Vertical integration: In an effort to control supply chain costs, Ingles owns and operates much of its warehousing, distribution, and transportation network. It also has a wholly-owned milk processing and packaging subsidiary, Milkco. In addition to supply assurance and cost control, Milkco generates third-party revenue. Milkco didn’t suffer physical damage from Helene but there was a water outage and a ban on water usage that continued for a few weeks after the hurricane that set the facility back.

Real estate footprint: Unlike most grocery chains that lease their stores, Ingles owns the property for 175 of its supermarkets, which include shopping centers in which Ingles in the anchor property. Serving as landlord in various shopping centers generates additional income for Ingles. Ingles also owns another 29 undeveloped sites, which may serve as eventual Ingles locations or other developments. Last July, my friends Lawrence Hamtil and Doug Ott appeared on the Flyover Stocks podcast to discuss outsized population and economic growth (listen here) in the southeastern U.S. Owning large tracts of real estate in a rapidly-growing region is an advantage when competitors are forced to pay higher rents to landlords.

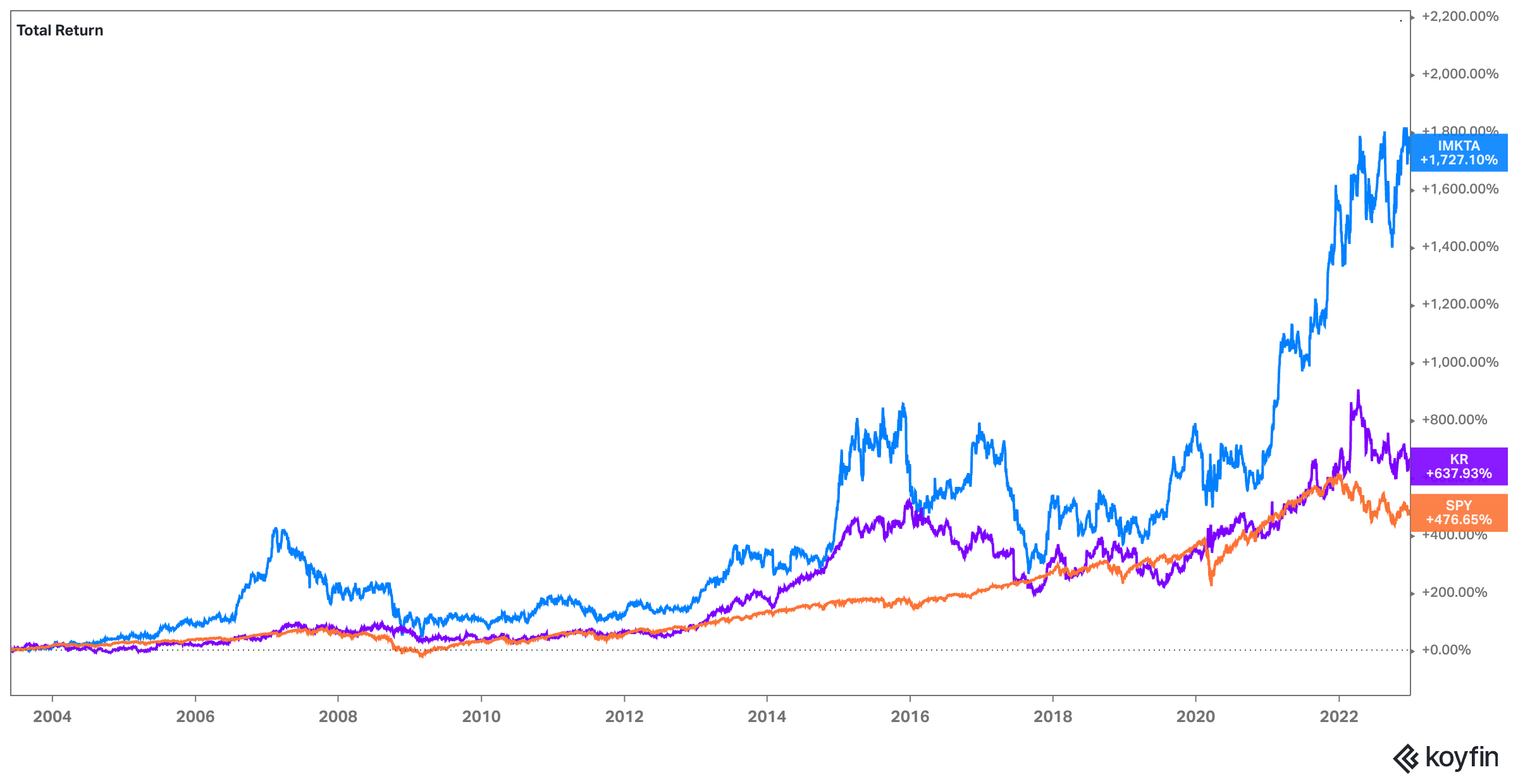

Family ownership: Robert Ingle was the third generation of a family of grocers and launched his own store in 1963. Today, his son, Robert Ingle II serves as chairman of the board and maintains 72.5% of the voting power between his Class A and Class B share ownership (as of the 2024 proxy). Family ownership and control can be good or bad for minority shareholders. On the one hand, family ownership tends to be longer-term focused, but it also risks being too conservative in times of rapid change. Prior to 2023, Ingles’s stock had a strong run (see below), but has lagged the market and its peers since.

According to Tenzing MEMO, the bull case on Ingles can be summarized as:

The market appears to discount the company’s earnings power and real estate value, possibly due to its low profile, limited analyst coverage, and lack of quarterly earnings calls. For value-oriented investors, this creates an opportunity to acquire a stable, cash-generative business at a discount to intrinsic value.

Tenzing MEMO’s “The Skeptic” feature, however, warns bulls to be cautious of a potentially deteriorating grocery business underneath the impressive real estate holdings. I agree that the focus of any potential Ingles investor should be on the quality of the underlying grocery operations. If that does well, the real estate should take care of itself.

The fact that Ingles doesn’t hold conference calls and doesn’t have analyst coverage, however, makes it particularly challenging for outside investors to keep tabs on the grocery business.

A scenario in which the real estate is monetized and unlocks value to minority shareholders is unlikely. Still, Ingles is an idiosyncratic business that’s worth digging into.

What are some SMID cap companies on your radar today? Let me know in the comments below.

Stay patient, stay focused.

Todd

Todd Wenning is the founder of KNA Capital Management, LLC, an Ohio-registered investment advisor that manages a concentrated equity strategy and provides other investment-related services.

At the time of publication, Todd, his immediate family, and/or KNA Capital Management, LLC or its clients owned shares of Wal-Mart.

Please see important disclaimers.

Landstar is a good Ensemble stock and I always enjoyed your write-up/video(s) on it. The biz model is great, but given how deep is the downcycle for trucking, I feel like a higher beta name like Heartland Express might generate higher risk adjusted return.

Ingles is cheap, but the land thesis has been busted in prior examples including Seritage, a Buffett name and he lost hundreds of millions. Catalyst has no time horizon of materialization. Leon’s Furniture at least has the catalyst there about land sale and redevelopment so I’d probably prefer that (no position though).

I agree that Imkta is content to let the grocery business muddle along. Many of their stores are deteriorating and losing business to competitors, but they continue to prioritize buying real estate over current operations.