Stocks on My Radar - Value Edition

Three ideas with forward P/E ratios below 11 times.

Todd Wenning is the founder of KNA Capital Management, LLC, an Ohio-registered investment advisor that manages a concentrated equity strategy and provides other investment-related services.

At the time of publication, the author, his immediate family, and/or KNA Capital Management, LLC or its clients have no positions (long or short) in the companies mentioned below

Please see important disclaimers.

In this edition of “stocks on my radar” I will highlight three overlooked or misunderstood businesses with forward P/E ratios well below the S&P 500’s 22x current forward P/E.

Each of these companies trades with a forward P/E of 11 or less - half that of the S&P’s. While they have enough quality factors to merit research, there’s a reason each of them are trading with those low multiples, so we’ll consider both the positives and the negatives.

First, we’ll look at a global customer experience operator quietly benefiting from AI-driven complexity rather than disruption.

Second, we’ll consider a spun-off healthcare supplier with durable cash flows masked by near-term dislocation.

Finally, we’ll analyze a niche industrial franchise emerging from legacy overhangs with improving capital allocation discipline.

The AI-driven research platform Tenzing MEMO is a tool I use for efficiency gains in my research process. As a solo investor, using Tenzing MEMO has helped me accelerate the initial research phase on new ideas and keep up with existing coverage by quickly synthesizing information.

Disclosure: Tenzing MEMO is a commercial partner and sponsor of this newsletter. I receive compensation or benefits if readers sign up using the promotional code. This section is an advertisement.

Nick and Tom at Tenzing MEMO are offering an exclusive trial for professional investors who use the FLYWITHUS code during signup. This code provides an extended 4-week trial (versus the standard 2-week trial) and six tickers to sample (versus the standard four).

I’ll feature some of Tenzing MEMO’s insights in this post alongside my own analysis. If you’re a professional investor interested in exploring its capabilities, you can find more information about the offer here. Please remember to use the FLYWITHUS code when you sign up to access the enhanced benefits.

IBEX Limited (IBEX)

In recent months, IBEX has regularly showed up on various screens I run. In my experience, that’s been a good signal that it’s time to take a closer look. There has to be something worth learning about.

My first job out of college with Vanguard was essentially a customer service role. I was a licensed registered representative, but the job was really about talking with 60 customers a day and helping them solve everything from simple to highly complex problems.

Having experienced the nuances involved in various customer service scenarios, I have a hard time believing that it will be fully replaced by AI anytime soon.

In other words, we’ll be saying “rep-re-sen-tat-ive” into our phones for many years to come.

Properly used, AI should empower the human customer service agents we work with to get better at solving the problem at hand.

In recent years, Washington, DC-based IBEX has pivoted from being a standard outsourced call-center company to fully integrating technology into the process. With 97% of its on-site workstations located outside of the U.S., the combination of lower-cost labor and technology can better serve clients and their customers.

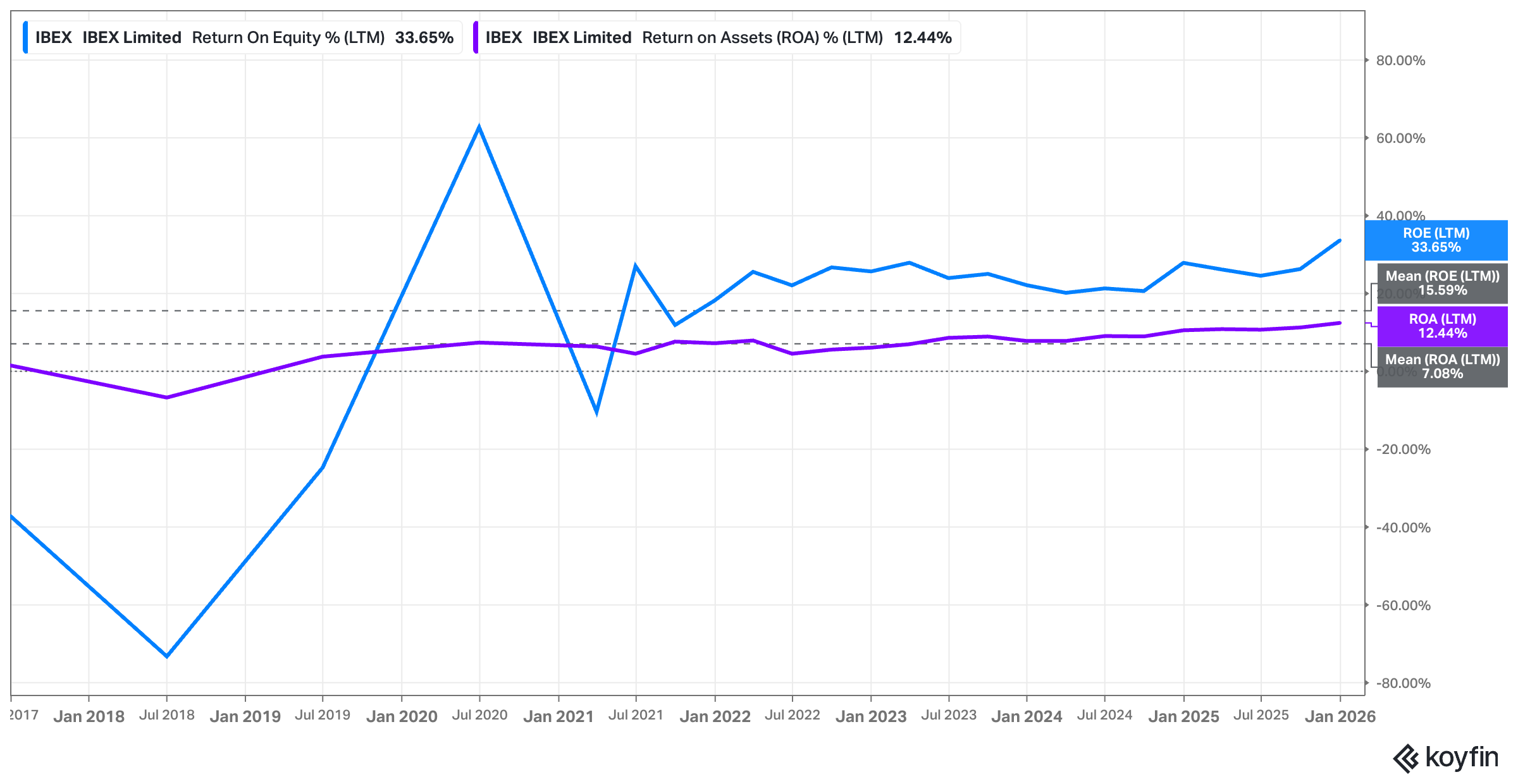

Customer service is a high turnover job. Getting yelled at half the day is draining. But IBEX has strong employee Net Promoter Scores (eNPS of 77) and high employee retention. It also appears to delight its clients, boasting a client eNPS of 71 and 98% client retention. As the above chart shows, these intangibles are showing up in the numbers.

But are the numbers durable? I asked Tenzing MEMO to help me determine IBEX’s primary moat source. It highlighted IBEX’s cost advantage and noted the following:

Delivery footprint tilted to lower-cost geographies. IBEX runs the vast majority of its operational capacity in offshore/nearshore markets (Philippines, Pakistan, Jamaica, Central America), and management disclosures show this mix has been increasing (e.g., ~97% of workstations outside the U.S. as of FY2025). That’s a structural labor cost advantage in a labor-heavy business.

Mix shift to higher-margin offshore work has been a key driver of margin expansion. In the FY2026 Q2 period (ended Dec 31, 2025), IBEX explicitly attributes improved margins to growth in higher-margin offshore regions; the 10-Q also discusses how shifting work from onshore to offshore tends to raise margin % even if it can reduce absolute revenue dollars.

Process + utilization leverage. Contact centers have meaningful fixed costs (sites, supervision, IT). Higher utilization improves unit economics. IBEX disclosures emphasize utilization and “site optimization” as a margin driver.

Critically, however, Tenzing MEMO added a key caveat:

In BPO [business process outsourcing], cost advantage is often shared across many competitors (everyone can operate in the Philippines, etc.). So this tends to be a “relative execution” advantage (who runs it better) rather than a hard structural barrier.

That’s important to keep in mind. With sufficient funds and time, it’s possible that someone could replicate the model. Replicating the culture could be more challenging, however. The low-cost advantage paired with a track record of delighting employees and clients might make IBEX more difficult to compete against than the average outsourced BPO.

Could a pure-play AI customer service offering fully disrupt IBEX? Maybe in time, but I continue to believe that there are certain situations where speaking with an actual human (supported by AI) will continue to be the superior brand interaction for both the customer and the client.

With a trailing 7% free cash flow yield, IBEX is worth a closer look. The next step in my research process would be to better understand its customer concentration risks. The top 25 customers account for 79% of revenue and the largest customer accounts for 10% of revenue. The loss of any one of these customers could be material.

Premium Flyover Stocks subscribers have exclusive access to the other two stocks on my radar. The content continues below.