Rotork Acquired for a Huge Premium

Industrial conglomerate ABB pays a pretty penny for the high quality industrial niche operator

Back in January 2025, I profiled Rotork plc (ROR.L), a nearly 70-year-old U.K. maker of mission-critical flow control actuators.

Today, ABB announced it plans to acquire Rotork in an all-cash deal at 503 pence per share, valuing Rotork at roughly $5.5 billion in enterprise value - a 73% premium to the previous day’s close.

Profile summary

Like every other Flyover Stocks profile, the Rotork report wasn’t a “buy” call. Using my moat, management, and forecastability framework, Rotork scored 3.0 out of 5, or middle of the pack relative to other companies I’d profiled.

That said, most of the demerits were due to a relatively new management team and low relative forecastability and simplicity scores, with Rotork selling into the oil & gas industry.

The moat, however, I found to be quite impressive - it scored a 4 in Moat Width and Depth.

A few things stood out enough to write about in January 2025:

Deep switching costs / cost of failure avoidance. Rotork’s actuators are a small fraction of the cost of the systems in which they’re installed, but failure is expensive. Once installed, customers don’t swap them out on price alone.

Best-in-peer-set returns on capital. At the time of the report, Rotork’s ROIC (~21%) was meaningfully ahead of the group I compared it against, including ABB (the acquirer), Emerson, and Flowserve.

A valuation that didn’t match the fundamentals. Rotork was trading at the bottom of its peer group on P/E and EV/EBITDA despite having margins and returns near the top of the group.

A newer leadership team not yet getting credit. CEO Kiet Huynh’s “Growth+” strategy was showing early results (double-digit revenue and profit growth in H1 2024) but hadn’t fully changed the market’s mind yet.

What surprised me

In the profile, I also flagged real reasons for caution, such as heavy oil & gas cyclicality, a run of management turnover through the 2010s, and low forecastability given currency and end-market swings. These factors kept me from buying the stock myself, along with the fact my portfolio was already overweight industrials.

Save a spike in the share price following the start of the US-Iran conflict, Rotork’s stock had been lackluster at best since last January, and multiples fell further recently as oil prices returned closer to pre-conflict levels.

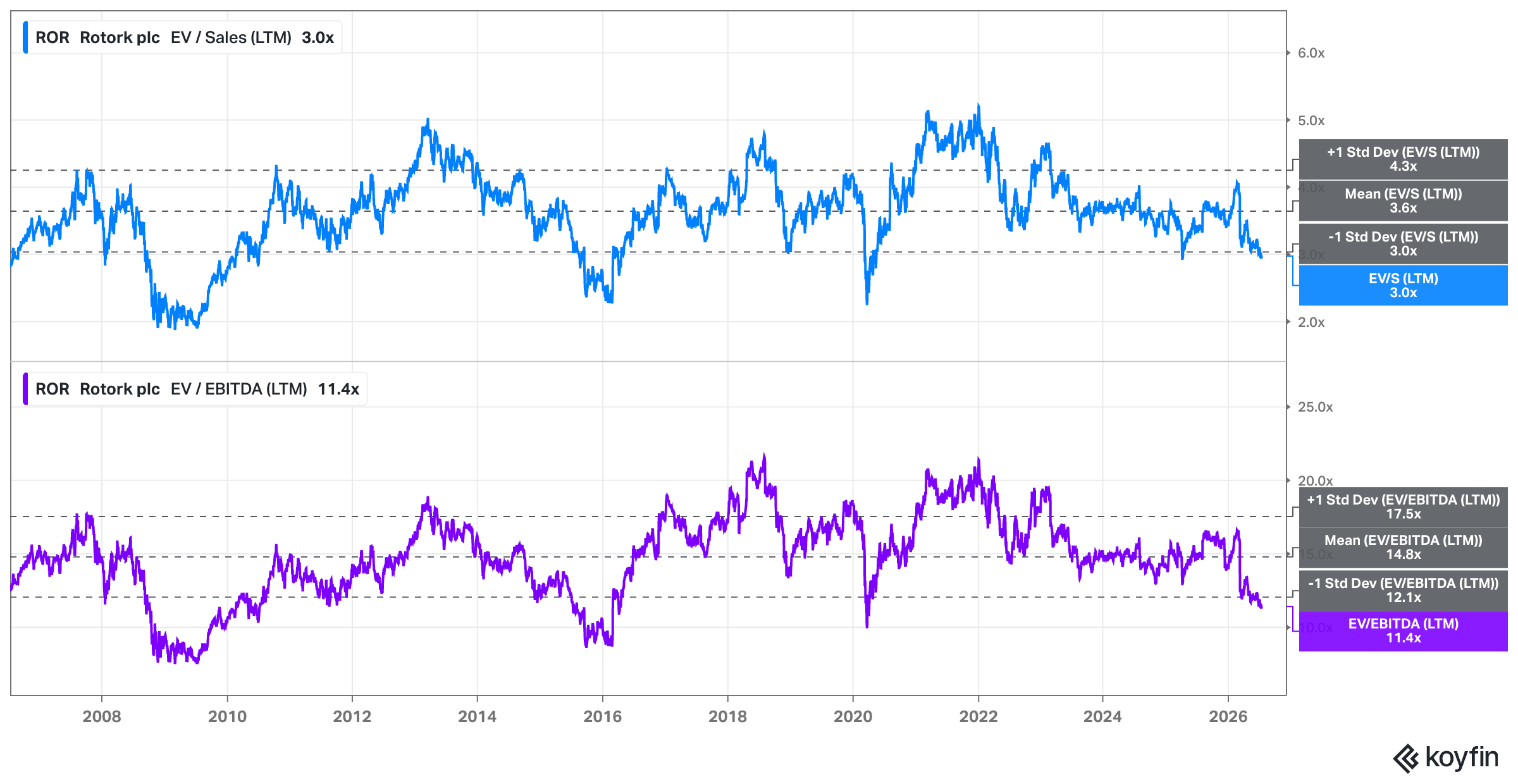

I’m less surprised that Rotork was acquired by a strategic buyer than I am the multiples ABB paid for Rotork - 5.3x revenue and 19.5x EBITDA, which are a considerable premium to the 20-year averages of 3.6x and 14.8x, respectively.

I would not have used those multiples to determine a fair price, but I noted in the original profile that:

With a starting free cash flow yield just under 5%, paired with the potential for high-single digit free cash flow per share growth (aided by mid- to high-revenue growth and some margin expansion), it’s an attractive setup to consider if you are looking for a quality mid-cap company in the global industrial space.

Good on Rotork for getting such an attractive offer. I’m not sure if there was an active auction for Rotork, but given the huge premium, I suspect there were competing bids.

The takeaway

I don’t write these profiles as buy recommendations. I write them to find durable, underappreciated businesses that I should keep on my radar. Writing them forces me as a portfolio manager to regularly compare the prospects of my current holdings against new ideas I may not have previously considered.

While Rotork didn’t find a place in my portfolios, this is a decent reminder that the gap between good business and cheap stock doesn’t stay open forever.

Stay patient, stay focused.

Todd

Todd Wenning is the President & CIO of KNA Capital Management, LLC, an Ohio-registered investment advisor that manages a concentrated equity strategy and provides other investment-related services.

At the time of publication, the author, his immediate family, and/or KNA Capital Management, LLC or its clients do not have positions in any company mentioned.

Please see important disclaimers.