A Tough March for These Flyover Stocks

Seven Flyover Stocks down 20%+ - what’s cyclical, what’s not, and how I’m ranking the opportunities

Todd Wenning is the President & CIO of KNA Capital Management, LLC, an Ohio-registered investment advisor that manages a concentrated equity strategy and provides other investment-related services.

At the time of publication, the author, his immediate family, and/or KNA Capital Management, LLC or its clients have positions in First Watch Restaurant Group.

Please see important disclaimers.

It’s been a tough March for many stocks, but a handful of previously profiled companies here at Flyover Stocks have had a particularly bad few weeks.

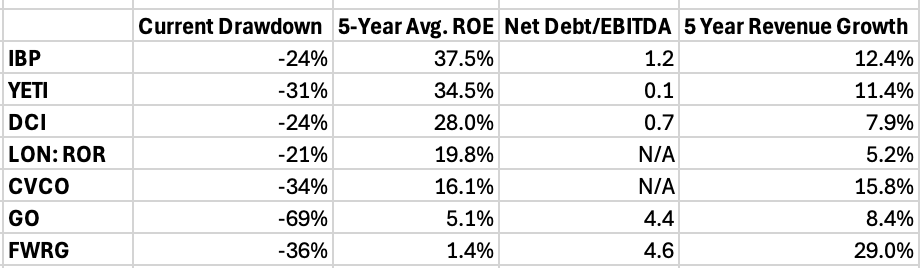

The following have all lost at least 20% of their value over the past month.

Grocery Outlet (GO)

YETI Holdings (YETI)

Cavco Industries (CVCO)

Donaldson (DCI)

First Watch Restaurants (FWRG)

Rotork (LON: ROR)

Installed Building Products (IBP)

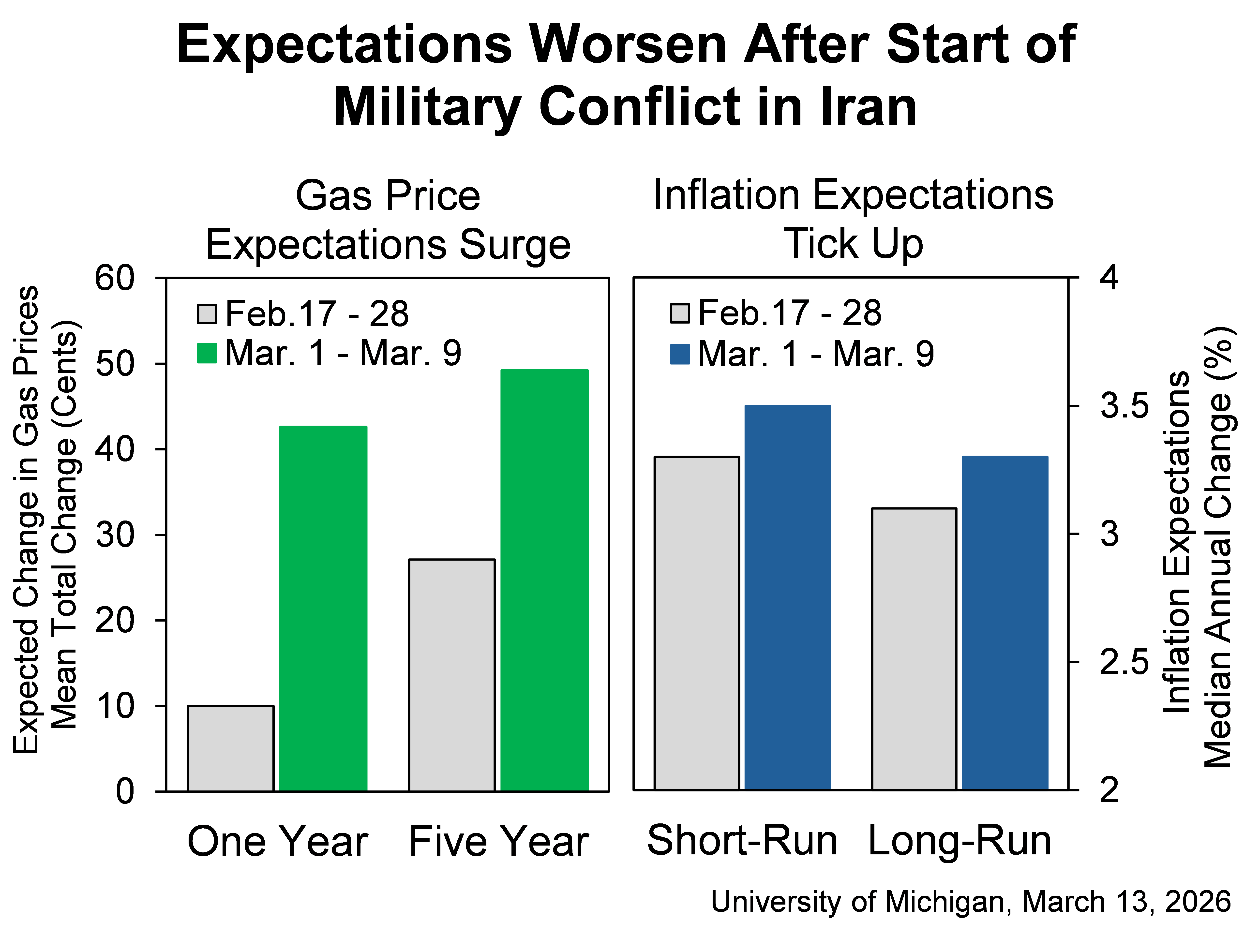

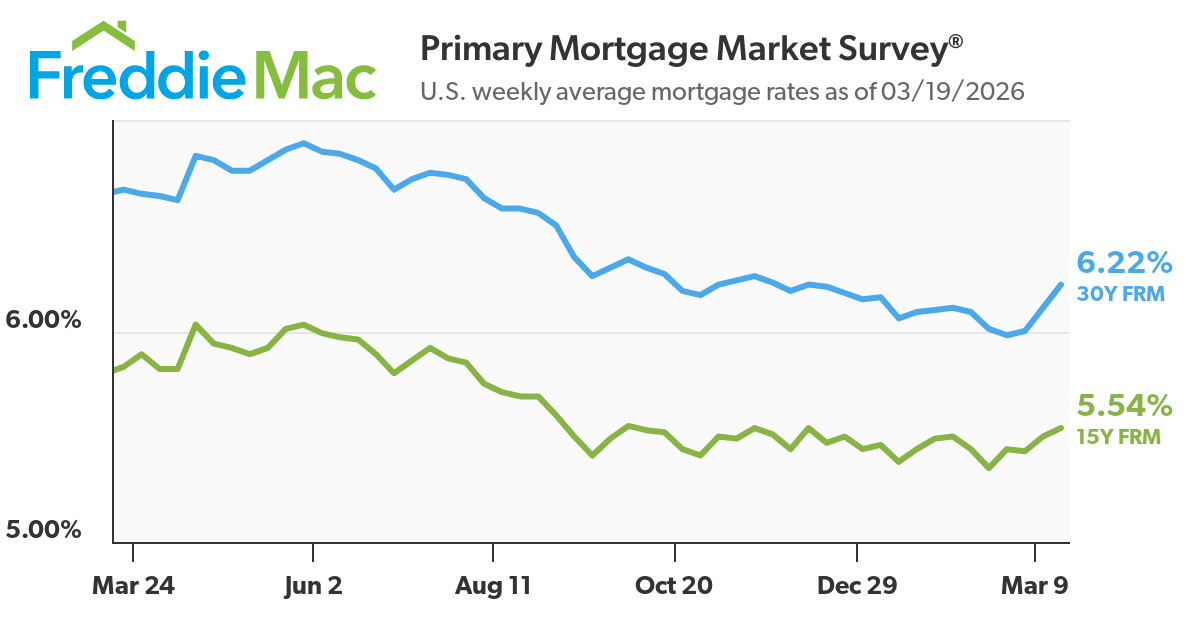

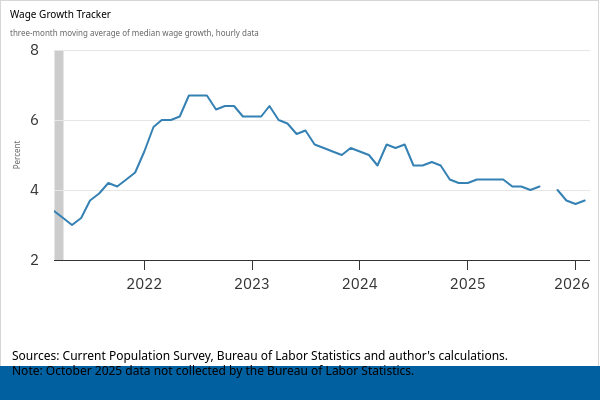

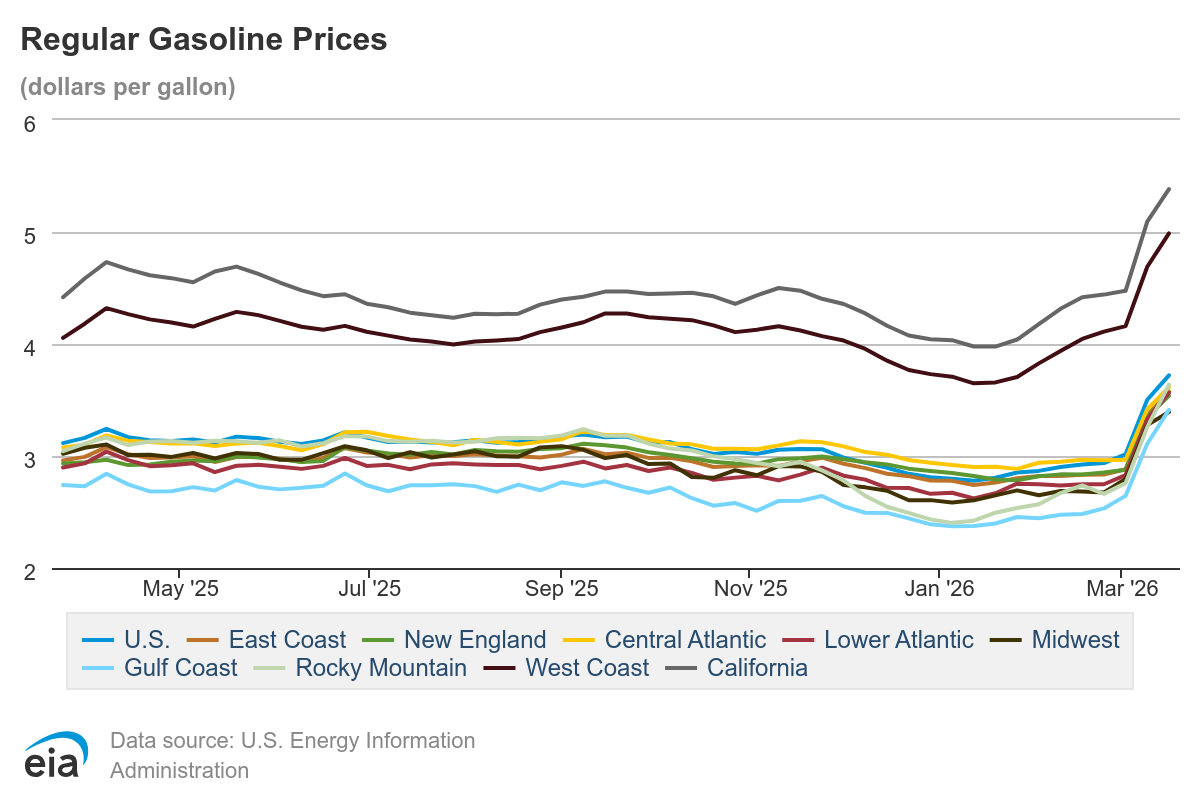

The common themes are exposure to consumer spending (GO, YETI, FWRG), housing (CVCO, IBP), and heavy industrial (DCI, ROR), all of which have shown weakness in recent weeks due to elevated interest rates, rising fuel prices, renewed tariff concerns, and higher expected inflation rates alongside declining wage growth.

What’s notable isn’t just that rates are high - it’s that multiple pressure points (fuel, utilities, financing costs, etc) are hitting at the same time, compressing discretionary spend faster than headline inflation suggests.

Here are some charts illustrating these trends:

US consumer confidence is shaky and that’s starting to show up in some of these results. Discretionary purchases like $200 coolers (YETI) and boozy brunches (FWRG) are harder sells when gas prices are spiking and utility bills outpace wage growth.

The math is straightforward - as non-discretionary expenses increase as a percentage of your paycheck, there’s less money left over for discretionary purchases. First Watch reported a 1.9% drop in fourth-quarter traffic and YETI noted a cautious wholesale environment as retailers don’t want to load up on inventory right now.

That same pressure is bleeding into housing demand as well, which is affecting Cavco and IBP - two companies that depend on new home construction activity.

The shaky consumer confidence environment should benefit Grocery Outlet, which sells overstocked grocery items at discounted prices, but the company has some operational troubles which have contributed to the recent drawdown. It’s been in the “penalty box” for the past year as I no longer think it qualifies as a Flyover Stock from a quality perspective. That said, I think it’s worth a closer look for turnaround-oriented investors.

Donaldson and Rotork are both in “transformational” periods, aiming to better line up their businesses for what they believe is the next phase of industrial project demand. Donaldson is preparing for a surge in power generation projects. Meanwhile Rotork’s “Growth+” strategy has been hamstrung by some deferred capital projects in midstream oil and gas due to geopolitical uncertainty and more restrictive financing.

With the exception of Grocery Outlet, I continue to believe these are six quality companies facing some cyclical rather than secular headwinds. In each case, the question isn’t “Is demand gone for good,” it’s, “When does it normalize, and what does the business look like when it does?”

Not all of these drawdowns are equal - some offer compelling opportunities for further research right now.

I’ve re-ranked all six based on research priority - and one name surprised me.

All paid subscribers (Flight Crew + Hangar), your content continues below.