A Fallen Angel Compounder with Zero Debt Balance Sheet

The company was a market darling during the COVID years but continues to have a number of secular long-term tailwinds.

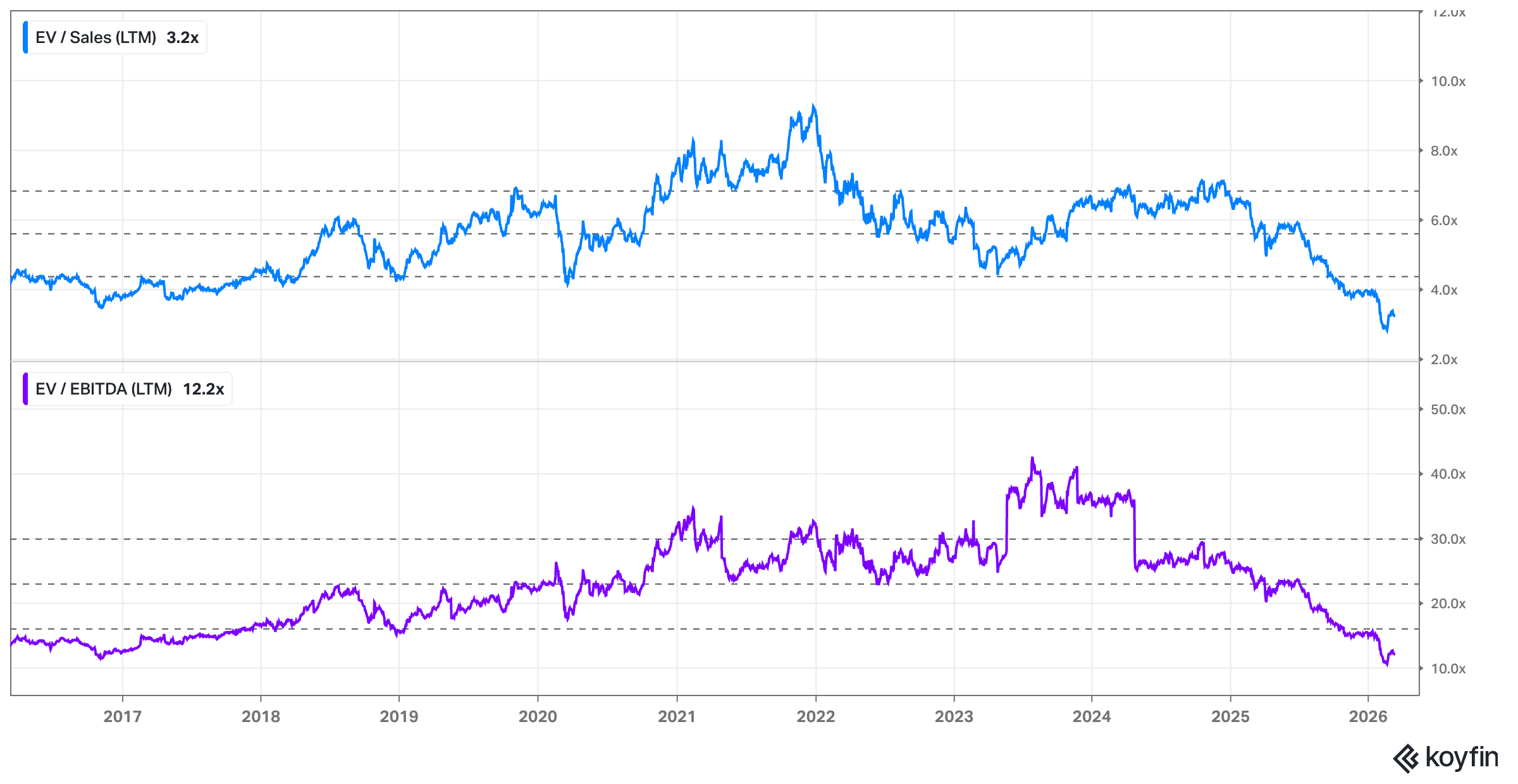

The past year has not been kind to many of the “compounder” stocks that were en vogue for much of the previous decade.

I’ve looked at a number of them over the last year and all their EV/EBITDA and EV/Sales charts tend to look something like this:

At their peak multiples, some of these businesses were priced to perfection. Investors assumed that continued high rates of earnings growth were inevitable.

Expensive quality has a dark side, however. When reality doesn’t match up with rosy implied expectations, the halo around a company fades and the shareholder base can turn from accommodating to skeptical. In some cases, it can even turn hostile.

But as any business owner knows, business isn’t always up and to the right. Reality doesn’t always match the expectations of others.

When fallen angels lose their halos (their multiples) but not their wings (still fundamentally strong), it can provide attractive opportunities for patient investors who have been waiting to buy at better prices.

The first quarterly Flyover Stock company profile takes a closer look at one of these fallen angels. This company still generates gobs of free cash flow, has a stewardship-minded management team, and stands to benefit from attractive long-term tailwinds.

(Oh, and it’s not a tech company.)

With a 6% free cash flow yield and zero financial debt, it’s a good time to take a fresh look at the opportunity.