5 Signs of a Flyover Stock

Here are a few characteristics of companies I aim to profile at Flyover Stocks

Audio version:

One of the benefits of experience as an investor is you start to pick up on patterns of attractive opportunities. Here are a few patterns I look for that pique my interest when flipping through new research ideas.

A funny or non-obvious name. Back in 2008, during the financial crisis’s early days, I ran many screens looking for quality businesses trading at low multiples. One company that kept popping up on the various screens was some tractor part distributor. I wasn’t interested in a tractor parts dealer, but I gave it a look since the name kept showing up. It turned out that it was a successful Tennessee-based retailer called Tractor Supply (TSCO). And while it did sell tractor parts, it was more focused on selling to hobby farmers in the exurbs and rural areas around cities. Regrettably, I held off buying on March 10, 2009, because the stock jumped 7% on the day and held off again as it surged 40% over the next month. I figured it would come back like most stocks had done in the previous few months. Nope. It’s up almost 3,400% since then, including dividends. I eventually bought some shares but missed out on a significant once-in-a-blue-moon opportunity. It’s a lesson that’s seared into my memory.

Source: Tractor Supply Headquartered outside of major cities. Jack Henry & Associates (JKHY) is a company with a non-obvious name that’s also located just about as far outside of a major city as you can get. Headquartered in Monett, Missouri (population 10,000), Jack Henry makes mission-critical banking software for small banks and credit unions around the U.S. To get to Monett is a three-hour drive south from Kansas City and four hours southwest from St. Louis. It was an especially unlikely stop for Wall Street analysts in the early days. The stock has generated 12.5% annualized returns over the last 20 years versus 9.7% annualized returns for the S&P 500 (both including dividends).

Monett, Missouri via Wikipedia Unglamorous work. The financial media is primarily concerned with companies doing transformational things (e.g. electric vehicles, AI) and those with mass market consumer products (e.g. Apple, Disney). But plenty of companies do important yet less glamorous work that are worth paying attention to. Badger Meter (BMI), for example, sells water flow measurement equipment into the residential and commercial utility markets and over the last ten years has outperformed both the S&P 500 and Nasdaq 100 by a wide margin.

Slow (but steady) growth. High growth and/or high returns on invested capital naturally attract competition and investor attention. On the other hand, slower-growth companies with lower but durable ROIC can fly under the radar for a long time. Packaging Corporation of America (PKG) is the third-largest containerboard producer in the U.S. Its top-line grew about 5% from 2012 to 2022 (including an acquisition of Boise Cascade) and posted low double-digit ROIC for most of the period, supported by an advantageous position in a rational oligopoly. Since September 2013, the stock has outperformed the S&P 500 by about 100 basis points per year on average.

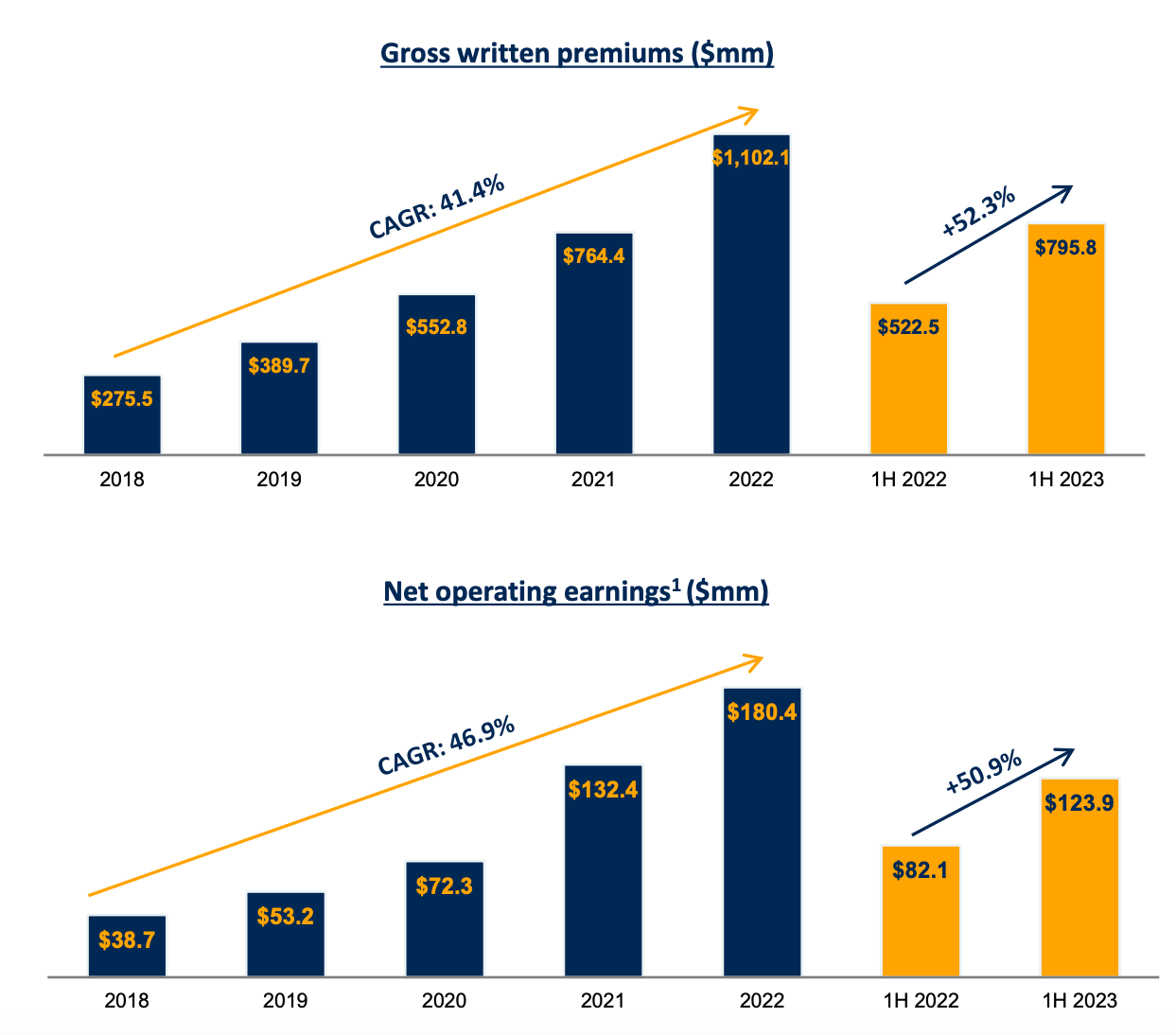

Source: Packaging Corporation of America Low/limited analyst coverage. Sell-side analyst coverage of a stock tends to follow institutional investor interest. Widespread institutional interest doesn’t happen if a stock is too small or doesn’t have enough liquidity. Until fairly recently Kinsale Capital (KNSL), an excess and surplus (E&S) insurance specialist, has largely flown under institutional investors’ and sell-side analysts’ radars despite being based in Richmond, Virginia, in close proximity with other major insurers, posting consistently strong growth in gross written premium and earnings, and having a differentiated business model. Eventually, the market catches onto exceptional fundamental performance and more investors and analysts have become interested in Kinsale.

It’s surprising how long some great companies can go overlooked in the market. While no company will check all five boxes above, I see each sign, in conjunction with their fundamental performance as a reason to further research a company.

Stay patient, stay focused.

Todd

All performance data as of September 8, 2023.

On the date of publication, Todd and/or his family owned shares of Kinsale Capital and Tractor Supply

Disclaimer:

This material is published by W8 Group, LLC and is for informational, entertainment, and educational purposes only and is not financial advice or a solicitation to deal in any of the securities mentioned. All investments carry risks, including the risk of losing all your investment. Investors should carefully consider the risks involved before making any investment decision. Be sure to do your own due diligence before making an investment of any kind.

At time of publication, the author or his family may have an interest in the securities mentioned or discussed. Any ownership of this kind will be disclosed at the time of publication, but may not be updated if ownership of a particular security changes after publication.

Information presented may be sourced from third parties and public filings. Any links to these sources are included for convenience only and are not endorsements, sponsorships, or recommendations of any opinions expressed or services offered by those third parties.

I've started researching Kinsale, and there's a lot to like about it !

I'd be interested to hear your thoughts about it.

My current understanding is that the multiples may be a little risky, especially if you exclude investments from net income and if the softening part of the cycle finally materializes. However, they've been warning about it for some time now, and E&S may prove a more resilient business line than others in the insurance landscape.